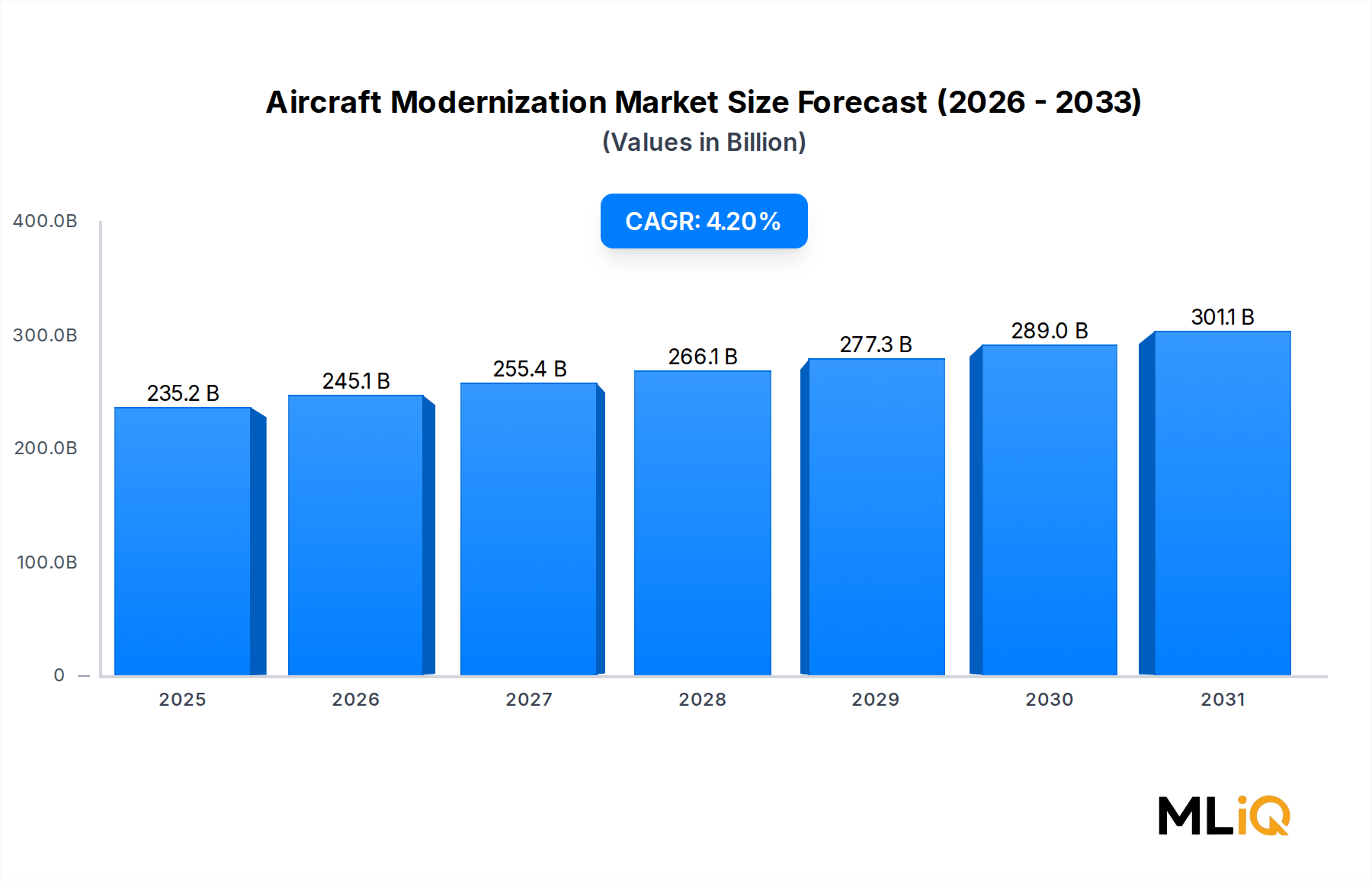

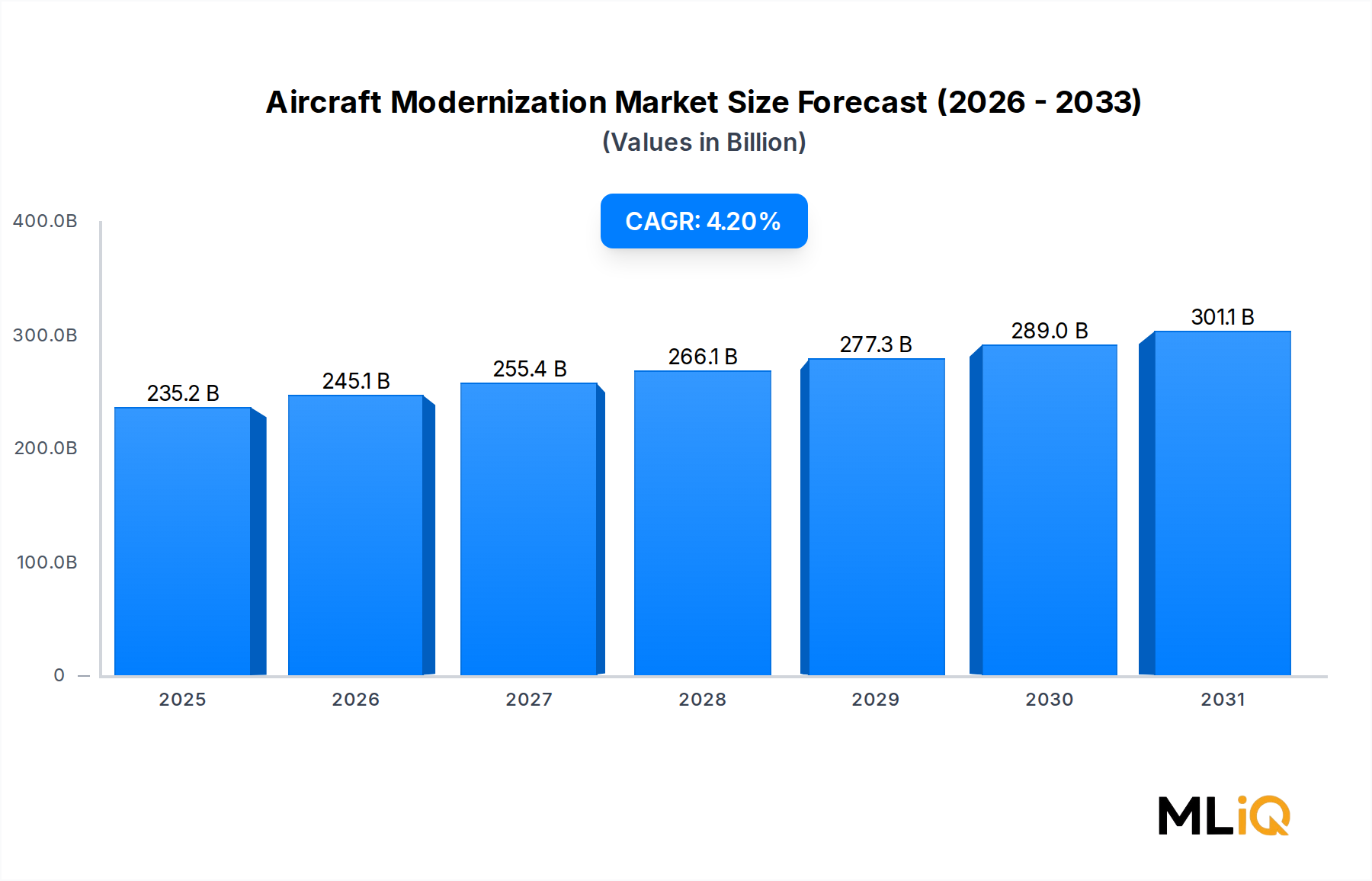

Combat Aircraft Dominance in the Aircraft Modernization Market

The combat aircraft sub-segment represents the single largest revenue-generating type within the Aircraft Modernization Market, commanding a disproportionate share of total program expenditure due to the high per-platform upgrade cost, the strategic imperative of maintaining air superiority, and the sheer volume of legacy fighter and attack aircraft fleets requiring continuous capability refresh across the world's major air forces.

Combat aircraft modernization programs are characterized by their technical complexity and multi-phase structure. A typical upgrade cycle for a fourth-generation fighter encompasses avionics architecture overhaul, radar cross-section management enhancements, electronic warfare system insertion, targeting pod integration, cockpit digitization, and compatibility with fifth-generation munitions. These programs frequently span five to ten years per aircraft class and involve prime contractors, government-owned maintenance depots, and a dense ecosystem of Tier 1 and Tier 2 sub-system suppliers.

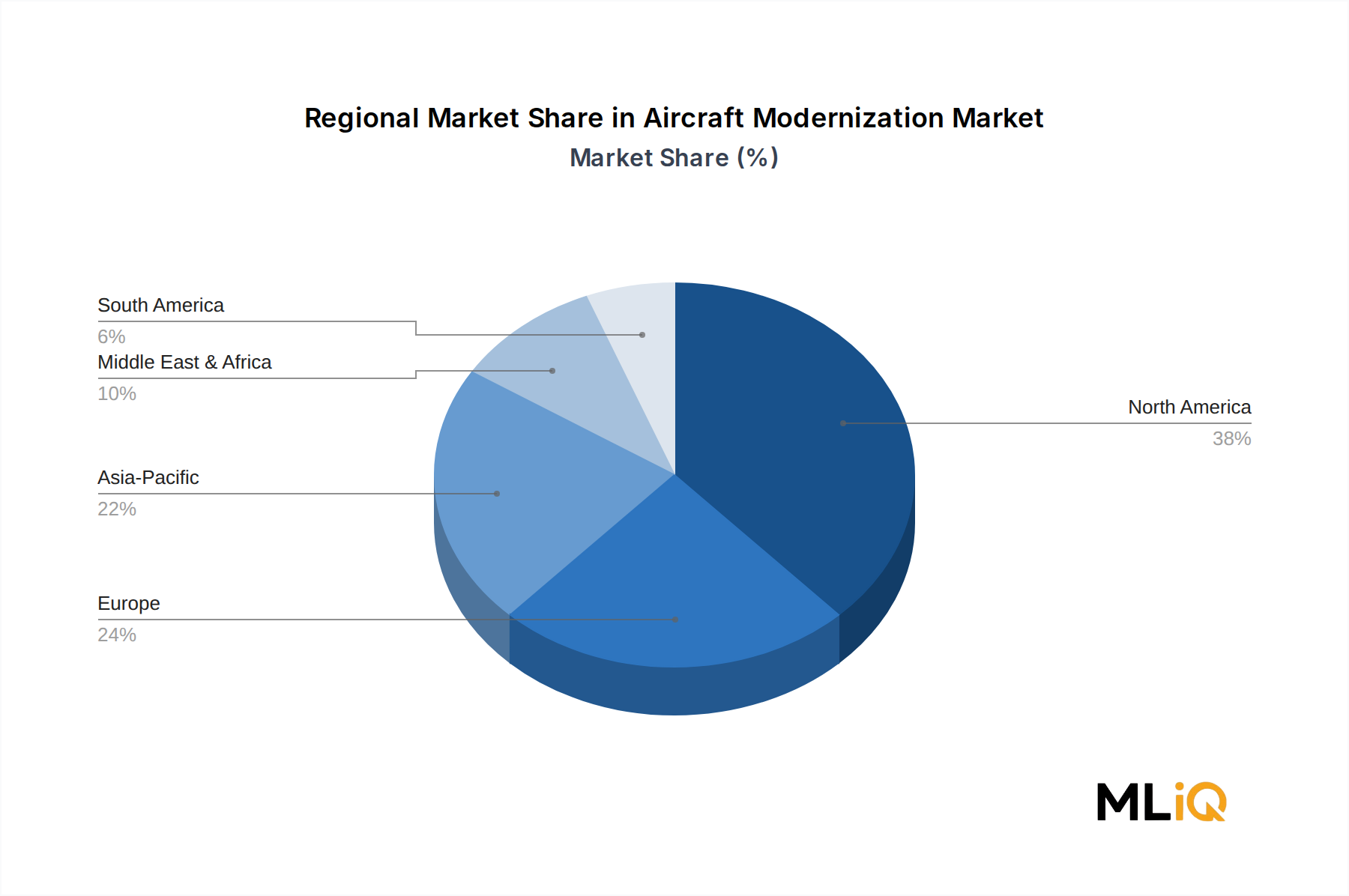

The United States Air Force's ongoing F-16 Active Service Life Extension Program, the U.S. Navy's F/A-18E/F Block III upgrade, and various international Mirage 2000 and Eurofighter Typhoon enhancement contracts collectively represent billions of dollars in backlogged modernization work. European NATO members, responding to revised defense expenditure commitments following the 2022 Russian invasion of Ukraine, have dramatically accelerated upgrade timelines for their legacy fleets, injecting urgency and incremental budgetary authority into programs that had previously been deferred or underfunded.

Lockheed Martin Corporation anchors the combat aircraft modernization ecosystem through its role as prime integrator for the F-16 Viper upgrade and its expanding international customer base for the F-35 sustainment and progressive capability delivery model. Dassault maintains a commanding position in Rafale and Mirage variant modernization, particularly across French, Indian, and Gulf state air forces. BAE Systems PLC drives significant revenue through Eurofighter Typhoon Phase Enhancement programs and legacy Tornado replacement integration work. Northrop Grumman contributes sensor fusion and electronic warfare capability insertions across multiple platforms.

The dominance of the combat aircraft sub-segment is reinforced by several structural factors. First, the geopolitical risk environment has elevated the political priority of air force readiness, making defense ministries more willing to allocate supplemental budgets for upgrade programs. Second, the unit economics of modernization are compelling: upgrading a proven platform to near-peer capability standards typically costs between 20% and 40% of the equivalent new-build acquisition price, making it fiscally attractive to defense finance authorities operating under constrained overall budgets.

Third, the industrial base is specifically configured to support this segment. Decades of investment in depot-level maintenance infrastructure, classified system integration facilities, and specialized avionics engineering talent have created significant barriers to entry that favor incumbent prime contractors. The Military Aircraft Upgrade Market, as a standalone vertical within the broader modernization ecosystem, reinforces this structural concentration by channeling defense procurement dollars toward proven upgrade integrators rather than new market entrants.

Growth within the combat aircraft sub-segment is expected to remain robust, with next-phase investments likely to emphasize artificial intelligence-assisted threat recognition, directed energy weapon pre-integration, and hypersonic weapon compatibility studies. The segment's share of total Aircraft Modernization Market revenue is projected to consolidate rather than expand, as commercial aviation modernization investment recovers, but its absolute dollar value is expected to grow consistently through the forecast horizon.