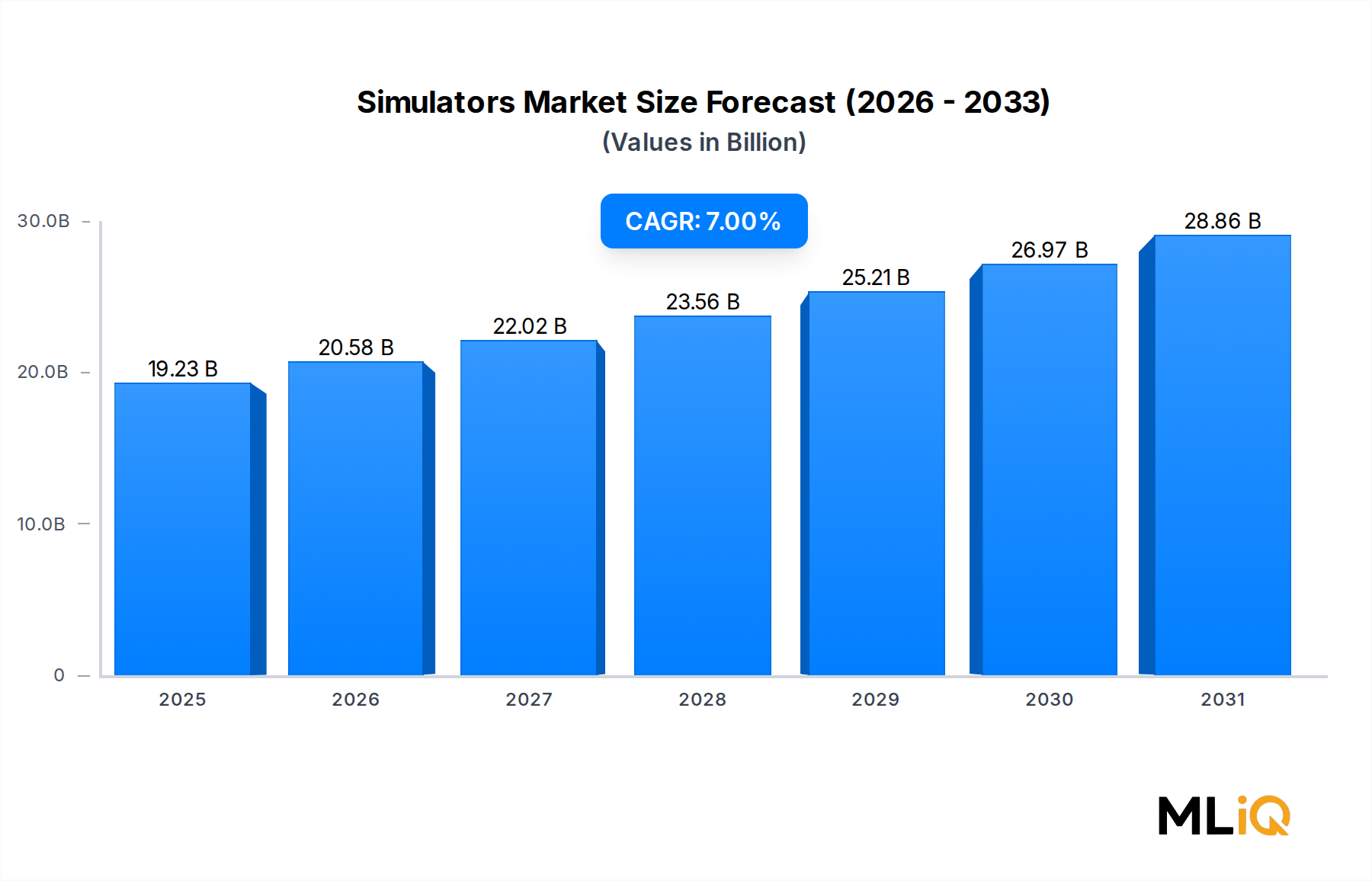

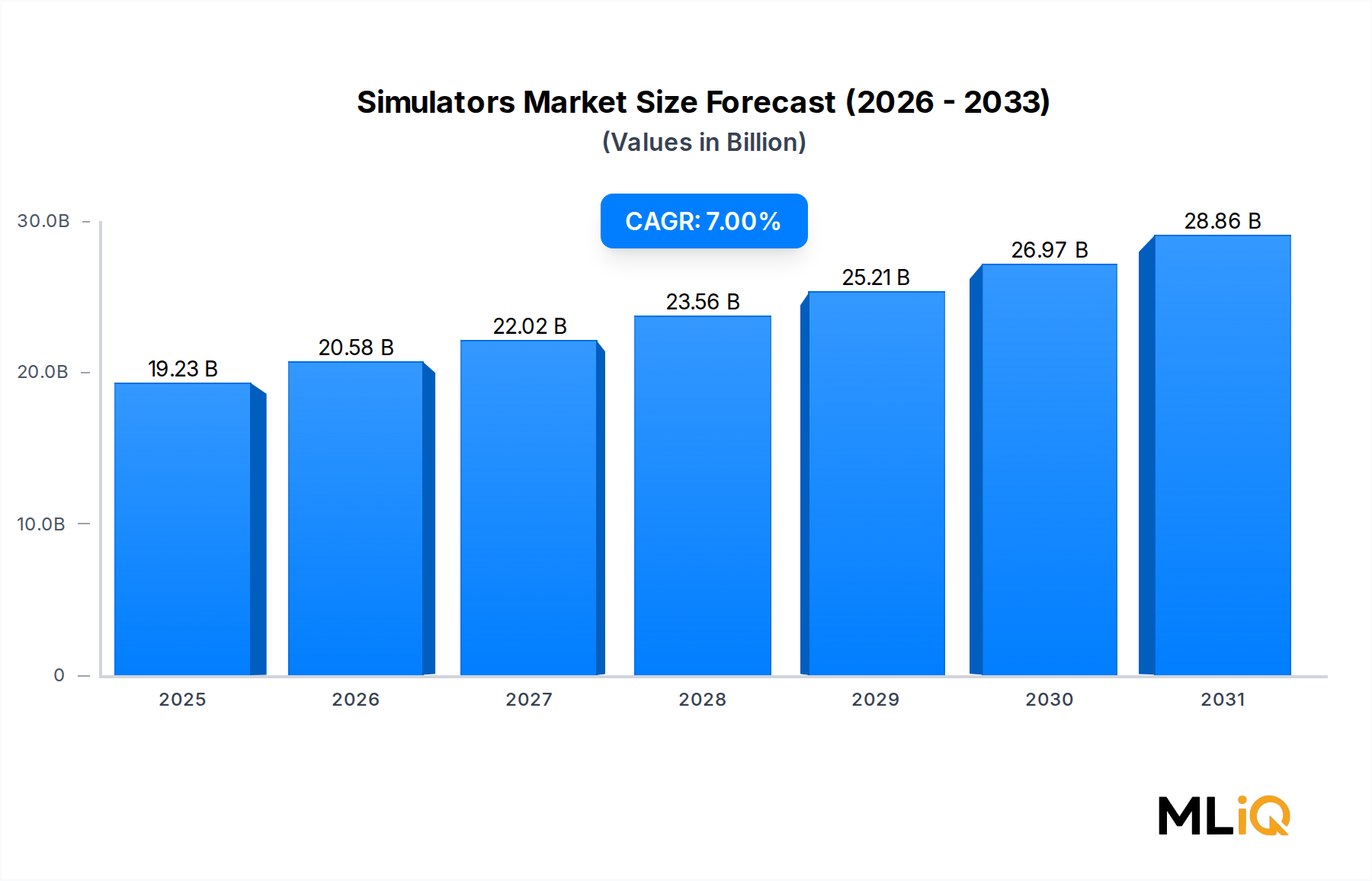

Demand Modeling & Market Estimation

Market sizing for the global Simulators Market across the 2026–2034 forecast period was computed through an integrated top-down and bottom-up modeling approach, with multi-level data triangulation applied at each segmentation layer (solution, platform, type, application, technique, and geography).

Bottom-Up Market Sizing — Key Metrics & Variables:

The bottom-up model was constructed by aggregating demand at the most granular unit level across all market segments. The following specific metrics were used as primary sizing variables:

- Number of Active & Qualified Simulator Units per Platform Type: Enumeration of in-service Full Flight Simulators (Level A–D), Flight Training Devices, Full Mission Bridge Simulators, and Land Forces Training Simulators by country and operator type, cross-referenced against FAA, EASA, and DoD certification databases — used to establish the installed base and replacement/upgrade cycle demand

- Pilot & Military Operator Training Hour Requirements per Annum: Regulatory minimum training hours mandated per pilot type (ATPL, CPL, MPL) and per military MOS/trade, multiplied by active operator headcount per country — used to model demand for simulator utilization time and capacity-driven procurement

- Average Unit Selling Price (ASP) by Simulator Category & Qualification Level: ASPs segmented by simulator type (e.g., Level D FFS: USD 10M–18M; FNPT II: USD 0.5M–2M; Full Mission Bridge Simulator: USD 3M–8M) derived from primary interviews with OEMs and procurement agencies — forming the revenue conversion layer of the demand model

- Defense Simulation Procurement Budget as % of Total Defense Expenditure: Derived from official DoD, NATO member state, and Asia-Pacific defense ministry budget documents, isolating the simulation and training systems allocation — used to model military training application revenue by country

Top-Down Validation:

The top-down approach commenced with total addressable market (TAM) estimation for global defense training & simulation spend and civil aviation training equipment spend, sourced from IMO, IATA, DoD, and NATO budget publications. These macro-level TAM figures were then disaggregated by platform (Airborne, Land, Maritime), application (Commercial, Military), and geography using verified demand distribution coefficients derived from primary research and institutional data.

Multi-Level Data Triangulation:

All market size estimates were triangulated across three independent data lenses:

- Supply-side triangulation — revenue reported by major simulator OEMs and service providers (reconciled via Bloomberg and PitchBook financials)

- Demand-side triangulation — training demand volumes and procurement pipeline data from government and regulatory sources

- Channel-side triangulation — distributor and training organization throughput data collected during primary interviews

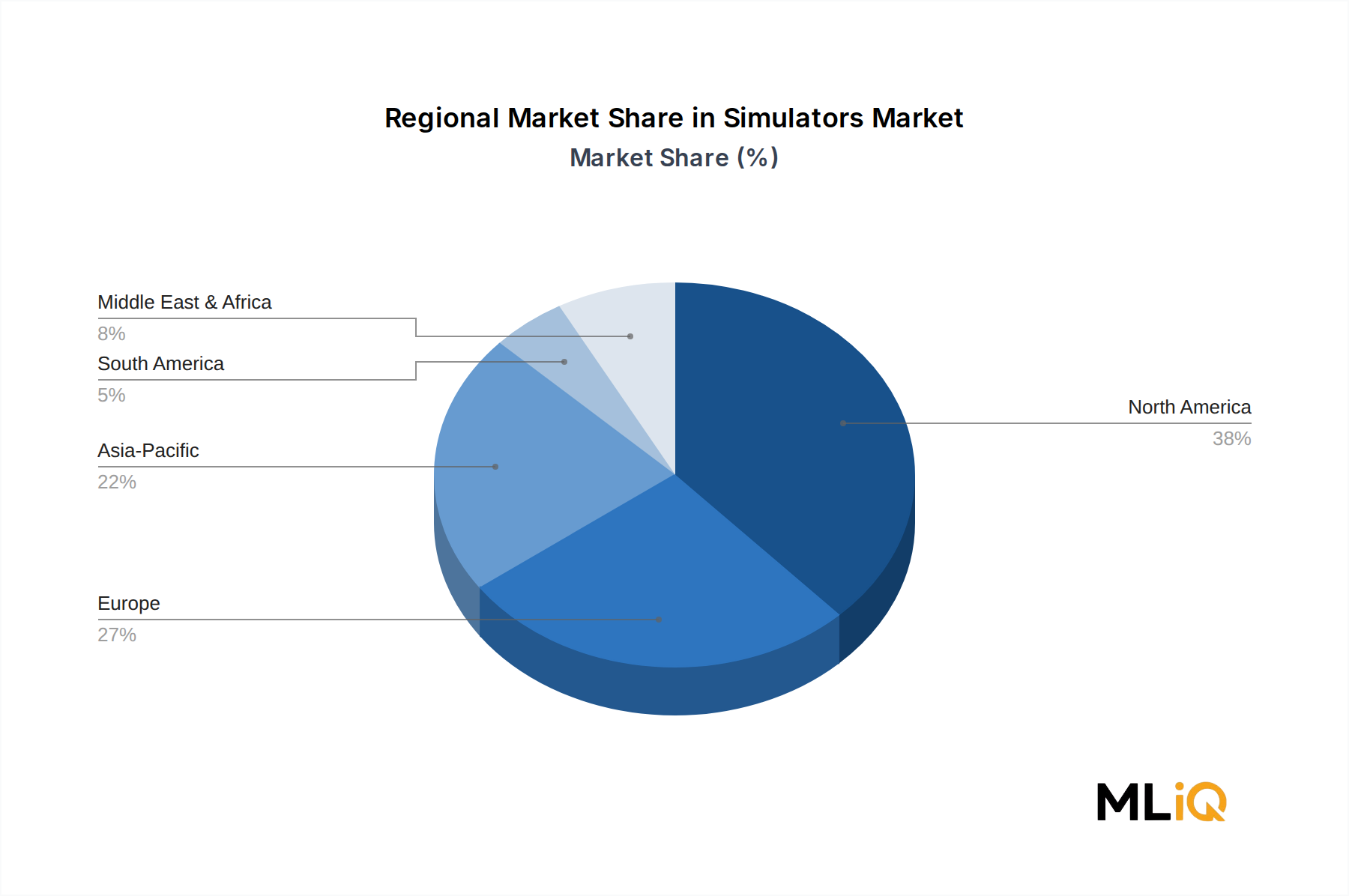

Regional estimates for North America, South America, Europe, Middle East & Africa, and Asia Pacific were validated through region-specific primary interviews and corroborated against country-level defense and aviation authority publications.