1. 繊維コーティング産業を形成している最近のM&A活動や製品発表にはどのようなものがありますか?

BASF SE、コベストロAG、アルケマグループなどの主要プレーヤーは、進化する最終用途の需要に応えるため、バイオベースおよび水性コーティング製剤に投資しています。化学メーカーと繊維OEM間の戦略的パートナーシップは、製品の商品化期間を加速させています。クラリアントとソルベイも、医療および輸送用途をターゲットとした機能性コーティングのポートフォリオを拡大しています。

+1 2315155523

Market Lens IQ は、国際市場に展開する組織に対し、高度なシンジケート調査レポート、カスタマイズされた業界分析、競合インテリジェンス、およびデータ主導のアドバイザリーソリューションを提供する、グローバルな市場インテリジェンスおよび戦略コンサルティング企業です。分析の卓越性とイノベーションへの強いコミットメントにより、Market Lens IQ は企業、投資家、コンサルタント、意思決定者に対し、競争の激しい業界における戦略的成長、業務効率化、および長期的なビジネス変革を推進するための実践的なインサイトを提供します。当社は、ライフサイエンス、消費財、半導体・電子機器、素材・化学、建設・製造、食品・飲料、エネルギー・電力、自動車・輸送、ICT・メディア、航空宇宙・防衛、BFSI(銀行、金融サービス、保険)など、幅広い業界を対象としています。深いドメイン専門知識と高度なアナリティクスを組み合わせることで、Market Lens IQ は進化するビジネス要件に合わせて調整された、包括的な市場評価、技術トレンド分析、投資インテリジェンス、サプライチェーンインサイト、価格分析、顧客行動調査、および将来の市場予測を提供します。

Market Lens IQ の機能の核心には、一次調査、二次調査、専門家インタビュー、データの三角測量、AIを活用したアナリティクス、およびリアルタイムの市場モニタリングを統合した、堅牢な360度調査方法論があります。当社の調査フレームワークは、業界データベース、企業情報のファイリング、政府刊行物、業界専門誌、規制枠組み、ホワイトペーパー、投資家向けプレゼンテーション、および世界的な経済指標を活用することにより、最高水準のデータ精度、信頼性、および戦略的妥当性を保証します。当社は、世界中の産業における新興市場の機会、破壊的テクノロジー、イノベーションエコシステム、競争のベンチマーキング、規制の変更、および高成長の投資セグメントを特定することに特化しています。顧客中心のアプローチにより、Market Lens IQ はスタートアップ、中小企業、多国籍企業、プライベートエクイティファーム、機関投資家、およびフォーチュン500企業と協力し、情報に基づいた意思決定と持続可能な競争優位性をサポートする高価値のビジネスインテリジェンスソリューションを提供します。継続的なイノベーション、デジタルインテリジェンス機能、および業界に焦点を当てた専門知識を通じて、Market Lens IQ は世界の市場調査およびコンサルティング業界における信頼できる戦略的パートナーとしての地位を確立し、組織が市場の複雑さを乗り越え、変革的な成長の機会を活用できるよう支援しています。

世界の繊維コーティング産業市場は、基準評価期間において**47.3億ドル**(約7,300億円)と評価されており、予測期間を通じて年平均成長率(CAGR)**3.85%**で拡大すると予測されています。この持続的な成長軌道は、構造的な需要の変化、進歩するポリマー化学、そして衣料品、輸送、医療、建設など複数の最終用途分野における幅広い応用範囲の収束を反映しています。

その根幹には、高機能繊維に対する規制および消費者の要求の高まりが市場を後押ししています。防護服、軍用生地、医療用繊維はすべて、特殊なコーティング化学品の需要増加を牽引しています。同時に、自動車内装、航空宇宙座席、船舶用内装材を含む輸送部門は、厳しい難燃性および耐摩耗性基準を満たす軽量で耐久性のあるコーティング生地を引き続き要求しています。

材料の観点から見ると、熱可塑性ポリマーは、リサイクル特性、加工の多様性、合成基布への優れた接着プロファイルにより、熱硬化性樹脂やゴムベースのシステムを上回り、主要な化学品セグメントを占めています。この優位性は、西ヨーロッパおよび北米のサプライチェーンで持続可能性に焦点を当てた調達ポリシーが浸透するにつれて、予測期間中に浸食されるのではなく、さらに強化されると予想されます。

マクロ的な追い風には、アジア太平洋地域における高機能衣料への一人当たり支出の増加、コーティングされたジオテキスタイルを必要とする政府のインフラ投資、および抗菌性および撥水性医療用生地の需要を牽引する世界的な医療分野の拡大が含まれます。さらに、電気自動車の成長は内装材の仕様を再構築し、軽量コーティングされたテクニカルテキスタイルに新たな需要ベクトルを生み出しています。

供給側では、市場は緩やかな統合を特徴とし、多国籍の特殊化学品メーカーが地域の配合業者と競争しています。BASF SE、Covestro AG、Solvay、Arkema Groupといった企業は幅広い製品ポートフォリオとグローバルな製造拠点を維持する一方で、Seyntex N VやTanatex Chemicals B Vのようなニッチプレーヤーは、配合の専門知識と用途に特化したカスタマイズで競争しています。

今後、市場はベースケースの仮定の下、2030年代半ばまでに**55億ドル**のしきい値を超える見込みです。主要な転換点には、溶剤ベースの化学品に対するREACHおよびEPA規制の厳格化が含まれ、これにより水性およびUV硬化型コーティングシステムへの移行が加速されるでしょう。バイオベースポリオール、グラフェン強化コーティング、相変化材料の統合に焦点を当てたイノベーションパイプラインは、早期参入者にとってプレミアムな価格設定機会とマージンの拡大を生み出すと予想されます。全体として、先進国と新興国の両方における永続的な需要の基礎に支えられ、見通しは引き続き堅調です。

熱可塑性樹脂サブセグメントは、ポリマータイプ別の繊維コーティング産業市場において、その機能的多様性と現代の高速繊維仕上げラインとの適合性の両方を反映した過半数のシェアを占め、収益的に優位なカテゴリーとして位置付けられています。ポリウレタン(PU)、ポリ塩化ビニル(PVC)、ポリアクリレート、熱可塑性ポリオレフィン(TPO)システムを含む熱可塑性コーティングは、柔軟性、耐薬品性、加工性のユニークな組み合わせを提供しており、現在、競合するポリマークラスは大規模にこれを再現できません。

熱可塑性樹脂の優位性は、いくつかの相互に関連する技術的および商業的利点に根ざしています。第一に、熱可塑性システムは本質的に再加工可能であり、製造業者が規格外の材料を回収・再生できるため、廃棄物を削減し、原材料コストを低減します。第二に、それらは調整可能な機械的特性を提供します。硬度、破断時伸び、引張強度は分子量の変化や可塑剤の配合を通じて調整でき、軽量スポーツウェア膜から頑丈な工業用防水シートまで幅広い用途に適しています。第三に、熱可塑性コーティングが織物と不織布の両方の基材と互換性があることで、その対象市場は不織布市場と伝統的な織物セグメントの両方に広がり、大幅に拡大します。

熱可塑性樹脂カテゴリー内では、ポリウレタンベースのコーティングが最大のサブカテゴリーであり、ポリウレタンコーティング市場で観察される広範なトレンドと一致しています。PUシステムは、優れた通気性、耐摩耗性、および美的表面品質により、高機能衣料、医療用繊維、自動車内装材で優位に立っています。VOC排出規制に牽引される水性PU分散液への世界的なシフトは特に顕著であり、原材料調達のダイナミクスを再構築し、ポリマー分散液市場のサプライヤーに新たな競争空間を開いています。

熱可塑性PVCコーティングは、可塑剤の懸念(特にフタル酸エステル系システム)により、ヨーロッパで規制当局の監視が厳しくなっているものの、バナーや日よけ用途、ジオメンブレン、および重い輸送用カバーで依然として優位を保っています。市場参加者は、規制地域でのコンプライアンスと市場アクセスを維持するために、非フタル酸エステル系可塑剤代替品やバイオベースPVC配合に積極的に投資しています。

熱可塑性樹脂セグメントを牽引する主要プレーヤーには、繊維コーティング用水性PU分散液で強力な地位を築いているCovestro AG、接着剤およびコーティング用途の両方に貢献するDispercollおよびElastollan製品ラインを持つBASF SE、および特殊繊維最終用途向けに設計されたPUポリマーを提供するThe Lubrizol Corporationが含まれます。Huntsman International LLCは、柔軟なポリウレタン用途を対象としたTEROLおよびRubinate製品ファミリーを通じて貢献し、Arkema Groupは高機能膜用途向けにKynarおよびPEBAX熱可塑性エラストマーラインを活用しています。

熱可塑性樹脂セグメントのシェアは単に維持されているだけでなく、統合が進んでいます。溶剤系熱硬化性システムに対する規制圧力と、EUグリーンディールフレームワークの下でのリサイクル可能で循環型繊維製品に対する需要の加速は、競合するポリマークラスを構造的に不利にしています。bluesign、OEKO-TEX、ZDHC MRSL準拠などの持続可能性認証は、ヨーロッパおよび北米のブランドアパレルサプライチェーンにおける購入の前提条件になりつつあり、熱可塑性水性システムは、これらの要件を満たす上で他の代替品よりも有利な位置にあります。その結果、熱可塑性樹脂セグメントは予測期間中に収益シェアを徐々に増やし、より広範な市場におけるリーダーシップを強化すると予想されます。

繊維コーティング産業市場は、明確に定義された一連の構造的ドライバーによって推進される一方で、意味のある規制上および運用上の逆風も乗り越えなければなりません。

ドライバー1:保護繊維の基準の向上。北米、ヨーロッパ、アジア太平洋地域の一部で、労働安全規制が大幅に強化されています。欧州PPE規則(EU)2016/425は、個人用保護具に対して厳格な性能試験を義務付けており、これは難燃性、耐薬品性、切断保護性を備えたコーティング生地の需要を直接的に高めます。保護服市場と密接に関連する世界の産業安全アパレルセグメントは、市場平均以上の速度で成長しており、高機能コーティング化学品に対する一貫した需要を生み出しています。石油・ガス、化学処理、建設などの分野では、コーティングされていない生地を認定されたコーティング代替品に置き換えることが数年来の長期的なトレンドとなっています。

ドライバー2:輸送部門の拡大。特にアジア太平洋地域における自動車生産量と、世界的な電気自動車製造の立ち上がりは、座席、ヘッドライナー、ドアパネル、貨物管理システムにおけるコーティングされたテクニカルテキスタイルに対する需要を増加させています。EVプラットフォームは、より重い従来の材料の代替として、軽量コーティングされた不織布複合材料の利用を増加させており、テクニカルテキスタイル市場のダイナミクスと交差しています。

ドライバー3:医療用繊維の需要。新興経済国におけるパンデミック後の医療インフラ投資は、抗菌性、撥水性、滅菌バリア性を備えたコーティング生地の需要を維持しています。世界的に処置量が回復しており、使い捨てコーティング医療用繊維の消費を牽引しています。

制約1:厳格な環境規制。主要な規制上の制約は、耐久性撥水(DWR)仕上げに使用されるパーフルオロアルキルおよびポリフルオロアルキル物質(PFAS)の継続的な制限と段階的廃止です。REACHに基づくEU PFAS制限提案と、米国におけるEPAの措置は、業界全体での再処方を強制しています。PFASベースの化学品に依存する企業は、準拠する代替品を開発するために多額の研究開発投資を迫られており、競争的な市場ダイナミクスによりコスト転嫁は制限されています。これは、規制リスクが競争環境を再構築しているフッ素ポリマーコーティング市場とも交差しています。

制約2:原材料価格の変動。イソシアネート、ポリオール、アクリルモノマー—繊維コーティング配合の主要な投入材料—は、石油化学原料の価格サイクルに左右されます。**2021**〜**2022**年の供給中断は、単一供給源調達戦略の脆弱性を露呈し、中堅配合業者のマージンを圧迫しました。

繊維コーティング産業市場の競争環境は、多角的なグローバル特殊化学品コングロマリットと、特化した地域配合業者の存在によって特徴付けられます。以下のプロファイルは、主要な参加者の戦略的ポジショニングを概説しています。

Arkema Group: アルケマ株式会社として日本法人を有し、フッ素ポリマーや高機能ポリマー分野で日本の産業に貢献。幅広いフッ素ポリマーおよび高機能ポリマーのポートフォリオを持つフランスの特殊材料企業。アルケマは、持続可能な繊維仕上げセグメントでシェアを獲得するため、バイオベースおよび低VOCコーティング技術に投資しています。

BASF SE: BASFジャパン株式会社として日本で事業展開し、繊維化学品を含む幅広いポートフォリオで日本の産業を支える。売上高で世界最大の化学品企業であり、分散液、バインダー、機能性仕上げ剤を含む包括的な繊維化学品部門を維持しています。BASFの水性コーティングプラットフォームは、ヨーロッパおよびアジアのアパレルおよびテクニカルテキスタイル製造で広く採用されています。

Clariant: クラリアントジャパン株式会社として、繊維助剤や機能性コーティング剤を提供し、日本市場で持続可能な化学ソリューションを展開。さまざまな機能性繊維添加剤とコーティング補助剤を提供するスイスの特殊化学品企業。クラリアントは、性能と環境コンプライアンスをターゲットとしたEcoTainラベル製品ラインを含む持続可能な化学イノベーションに注力しています。

Covestro AG: コベストロ ジャパン株式会社として、水性ポリウレタン分散液など高性能ポリマー材料を日本の繊維産業に供給。高性能ポリマー材料の世界的な主要メーカーであり、コベストロのDispercollおよびImpranil水性PU分散液ラインは、繊維コーティングにおける業界ベンチマークです。同社は、マスバランスおよびバイオアトリビュート原材料イニシアチブを通じて循環型経済ロードマップを加速しています。

Huntsman International LLC: ハンツマンジャパン株式会社を通じて、繊維加工用化学品やポリウレタン中間体を提供し、日本市場の持続可能性を追求。テキスタイルエフェクトおよびポリウレタン部門を通じて事業を展開し、コーティング中間体および機能性仕上げ化学品を提供しています。同社はAviteraおよびTEROLブランドの下で持続可能な製品ポートフォリオの拡大に積極的に取り組んできました。

Solvay: ソルベイ・ジャパン株式会社として、フッ素ポリマーや高機能コーティングシステムを提供し、日本の先端材料分野に貢献。フッ素ポリマーベースおよび高機能コーティングシステムを提供するグローバルな先進材料および特殊化学品グループ。ソルベイは、次世代フッ素フリーバリア技術への投資により、PFAS規制の移行を乗り越えようとしています。

The Lubrizol Corporation: ルーブリゾール・ジャパン株式会社として、高性能ポリウレタンポリマーや繊維コーティング樹脂を提供し、日本の高機能アパレル・医療用繊維を支える。バークシャー・ハサウェイの子会社で、EstaneおよびSancureブランドのもとで設計されたPUポリマーと繊維コーティング樹脂を提供しています。ルーブリゾールは、世界中の高機能アパレルおよび医療用繊維コーティング用途における主要なイネーブラーです。

Formulated Polymer Products Ltd: テクニカルテキスタイル用途向けポリマーベースコーティングの専門配合業者であり、強力なアプリケーションエンジニアリング能力により、工業用、保護用、輸送用最終用途向けのカスタマイズソリューションを提供しています。

Impreglon UK Limited: テクニカルテキスタイルおよびエンジニアリングコンポーネント向けの工業用コーティングサービスを専門とする英国企業。独自の表面処理能力で航空宇宙、自動車、工業用生地の最終市場にサービスを提供しています。

Seyntex N V: 保護用および工業用アプリケーション向けに高性能コーティング生地を開発・製造するベルギーのテクニカルテキスタイル専門企業。Seyntexは、特殊PPE市場向けの統合された生地およびコーティング開発で差別化を図っています。

SRF Limited: 柔軟なパッケージングおよび工業用用途向けコーティング生地生産で強力な地位を占めるインドの多角的な化学品およびテクニカルテキスタイルコングロマリット。SRFは、インドでの低コスト製造と輸出能力の成長から恩恵を受けています。

Tanatex Chemicals B V: 繊維助剤と機能性コーティングに特化したオランダの特殊化学品企業。Tanatexは、持続可能な配合化学と、ミルパートナーとの密接なアプリケーション開発協力を重視しています。

2023年1月:Covestro AGは、アウトドア高機能アパレルにおける透湿性メンブレン用途向けに特別に設計された次世代水性ポリウレタン分散液の商用発売を発表し、PFASフリーのDWR代替化学品をターゲットにしています。

2023年3月:BASF SEは、自動車およびアパレル最終用途におけるパンデミック後の需要回復に牽引されたヨーロッパ市場での供給逼迫に対応するため、ルートヴィヒスハーフェン工場における繊維グレードアクリルバインダーの生産能力を**15%**拡大しました。

2023年6月:Arkema Groupは、特殊バイオベースポリオール生産者の買収を完了し、循環型経済のコミットメントに合致する持続可能なポリウレタン繊維コーティング配合向けの上流統合を強化しました。

2023年9月:Clariantは、ITMAバルセロナ展示会でZDHC MRSLレベル3準拠の新しい機能性コーティング添加剤ラインを発表し、世界のブランドアパレルサプライチェーン向け準拠化学品における同社の地位を強化しました。

2023年11月:Huntsman International LLCは、主要なアジアの合成繊維メーカーと戦略的供給契約を締結し、EV内装繊維用水性PUコーティングシステムを共同開発することで、自動車の電化と繊維イノベーションの交差の拡大を反映しています。

2024年2月:Solvayは、保護服向けのフッ素フリー高性能バリアコーティングを開発するために、欧州の研究コンソーシアムとの協力を発表しました。これは、REACHに基づくEU PFAS規制提案に対する広範な業界の対応の一環です。

2024年4月:SRF Limitedは、ラジャスタン州の施設で新しいコーティングされたテクニカルテキスタイルラインを稼働させ、中東およびヨーロッパ市場からの輸出需要の増加に対応するため、年間生産能力を**20,000トン**増加させました。

2024年8月:The Lubrizol Corporationは、Sancure水性PU分散液製品ファミリーのライフサイクルアセスメントデータを公開し、溶剤系同等品と比較して炭素排出量を**32%**削減したことを実証し、顧客の持続可能性報告要件を支援しています。

繊維コーティング産業市場は、成長率、需要ドライバー、競争強度が地域によって大きく異なる、明確な地域ダイナミクスを示しています。

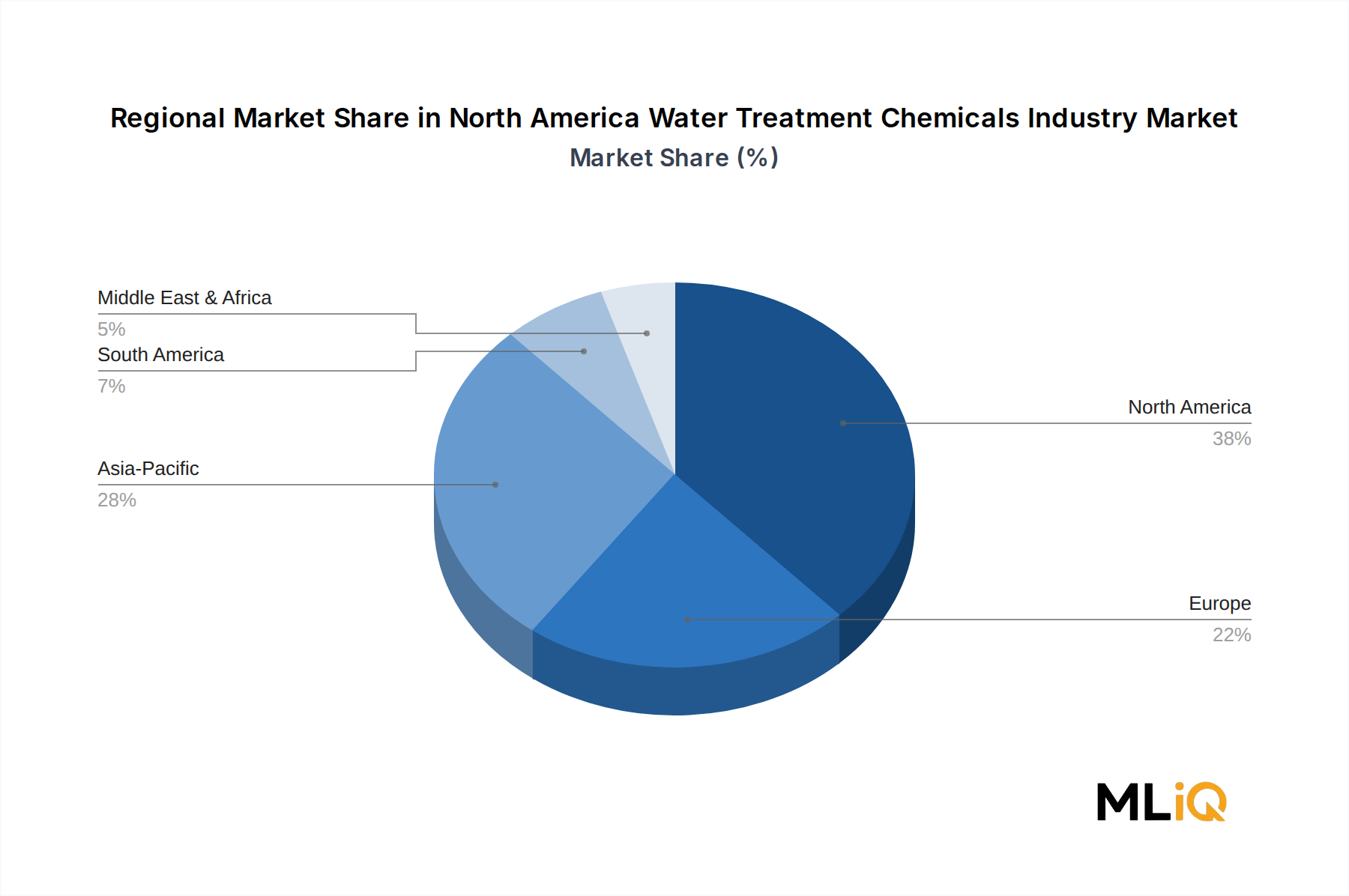

アジア太平洋地域は、推定で世界の収益の**42〜45%**を占める、最大かつ最も急速に成長している地域市場です。中国は、その大規模な統合された繊維・アパレル製造拠点、急速に拡大する自動車生産、およびコーティングされたジオテキスタイルを必要とする国内インフラ投資の増加に牽りされ、需要の中心であり続けています。インドは、国家テクニカルテキスタイルミッション(NTTM)の下での政府支援スキーム、国内PPE製造の増加、および輸出志向型のアパレル部門の成長に支えられ、地域内で最も急速に成長している国別市場です。この地域のCAGRは、製造コストの優位性、中間層消費の拡大、および産業安全規制導入の増加に支えられ、世界の平均を上回る約**4.8〜5.2%**と推定されます。

ヨーロッパは最も成熟した地域市場であり、世界の収益の約**28〜30%**を貢献しています。需要は品質とコンプライアンス志向によって特徴付けられ、REACH規制、OEKO-TEX、およびbluesign認証がコーティング化学品の高級化を推進しています。ドイツ、フランス、イタリア、英国が主要な消費の中心地です。CAGRは推定で**2.5〜3.0%**と緩やかであり、製造コスト圧力とアパレル生産のアジアへの継続的な移転によって制約されています。しかし、ヨーロッパは持続可能でバイオベースのコーティング技術の主要なイノベーションハブであり続け、EUのエネルギー効率建築基準によって推進される建設セグメントは、コーティングされた建築用メンブレンを通じて安定した需要の基盤を提供し、防水膜市場およびより広範な特殊化学品市場と交差しています。

北米は世界の市場価値の約**18〜20%**を占め、米国が地域の需要を支配しています。主要なドライバーには、高性能コーティング生地の軍事・防衛調達、医療用繊維生産、および産業・ろ過用途における機能性コーティング市場の成長が含まれます。この地域のCAGRは**3.2〜3.5%**と推定されます。カナダとメキシコはわずかに貢献しており、メキシコのマキラドーラ繊維部門は、ニアショアリングトレンドに関連する成長機会を提示しています。

中東・アフリカおよび南米は合わせて世界の収益の残りの**8〜12%**を占めます。中東は建設活動によって段階的な成長が見られ、ブラジルが牽引する南米は、国内アパレル製造および農業用ジオテキスタイル需要から恩恵を受けています。

日本は繊維コーティング産業において、アジア太平洋地域の主要な市場の一つです。世界市場は現在47.3億ドル(約7,300億円)と評価されており、アジア太平洋地域がこのうちの約42〜45%を占めるとされています。日本市場は、このアジア太平洋市場の一部として、高機能製品や環境配慮型製品に特化した成長が見込まれ、その規模は数千億円規模と推定されます。日本経済の特性として、技術革新への強い志向、高齢化社会における医療・ヘルスケア分野の重要性、そして自動車産業、特に電気自動車(EV)へのシフトが、高機能繊維コーティングの需要を牽引しています。国内市場の成長率は成熟市場であるため、新興国ほど高くはないものの、高付加価値製品や環境配慮型製品への投資が継続的に行われています。

日本市場における主要なプレーヤーとしては、BASF SE(BASFジャパン)、Covestro AG(コベストロ ジャパン)、Arkema Group(アルケマ)、The Lubrizol Corporation(ルーブリゾール・ジャパン)、Solvay(ソルベイ・ジャパン)、Clariant(クラリアントジャパン)、Huntsman International LLC(ハンツマンジャパン)などの多国籍企業が、その日本法人を通じて存在感を示しています。これらの企業は、高性能ポリマー材料や持続可能なコーティング技術を提供し、日本の繊維産業を支えています。規制および標準化の枠組みとしては、JIS(日本産業規格)が品質基準として広く適用されています。特に、製品の安全性や環境適合性に関する基準が厳しく、化学物質の審査及び製造等の規制に関する法律(化審法)が関連化学物質の取り扱いを規定しています。また、世界的なサプライチェーンにおいて、国際的な持続可能性認証の遵守が、日本企業にとっても重要な要件となっています。PFAS(有機フッ素化合物)に関する世界的な規制強化の動きは、日本国内でも代替技術の開発と導入を促進しています。

日本における繊維コーティングの流通チャネルは主にB2Bであり、化学品メーカーから繊維加工業者、最終製品メーカーへと供給されるのが一般的です。専門商社が国内外の化学品を日本の製造業に供給する役割も大きいです。日本市場の消費者は、最終製品において高い品質、安全性、耐久性、そして近年では環境性能を重視する傾向があります。特に、アウトドアアパレル、医療用繊維、自動車内装材といった分野では、価格よりも性能やブランド価値が購買決定要因となることが多く、これが高機能・高付加価値なコーティング製品の需要を後押ししています。EVの普及に伴い、軽量で高耐久性、かつ環境に配慮した内装材への需要が高まっていることも特筆すべき点です。

本セクションは、英語版レポートに基づく日本市場向けの解説です。一次データは英語版レポートをご参照ください。

| 項目 | 詳細 |

|---|---|

| 調査期間 | 2020-2034 |

| 基準年 | 2025 |

| 推定年 | 2026 |

| 予測期間 | 2026-2034 |

| 過去の期間 | 2020-2025 |

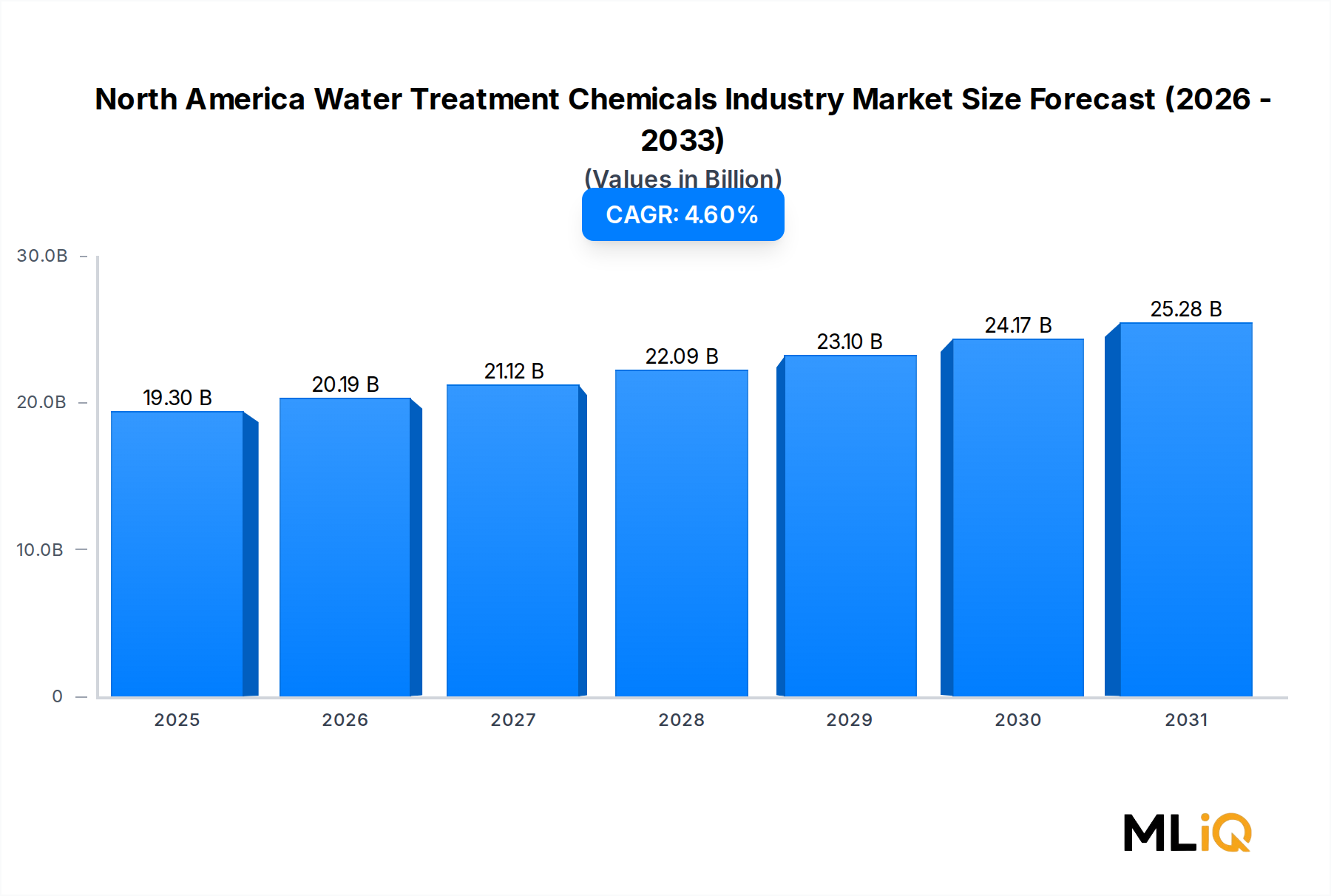

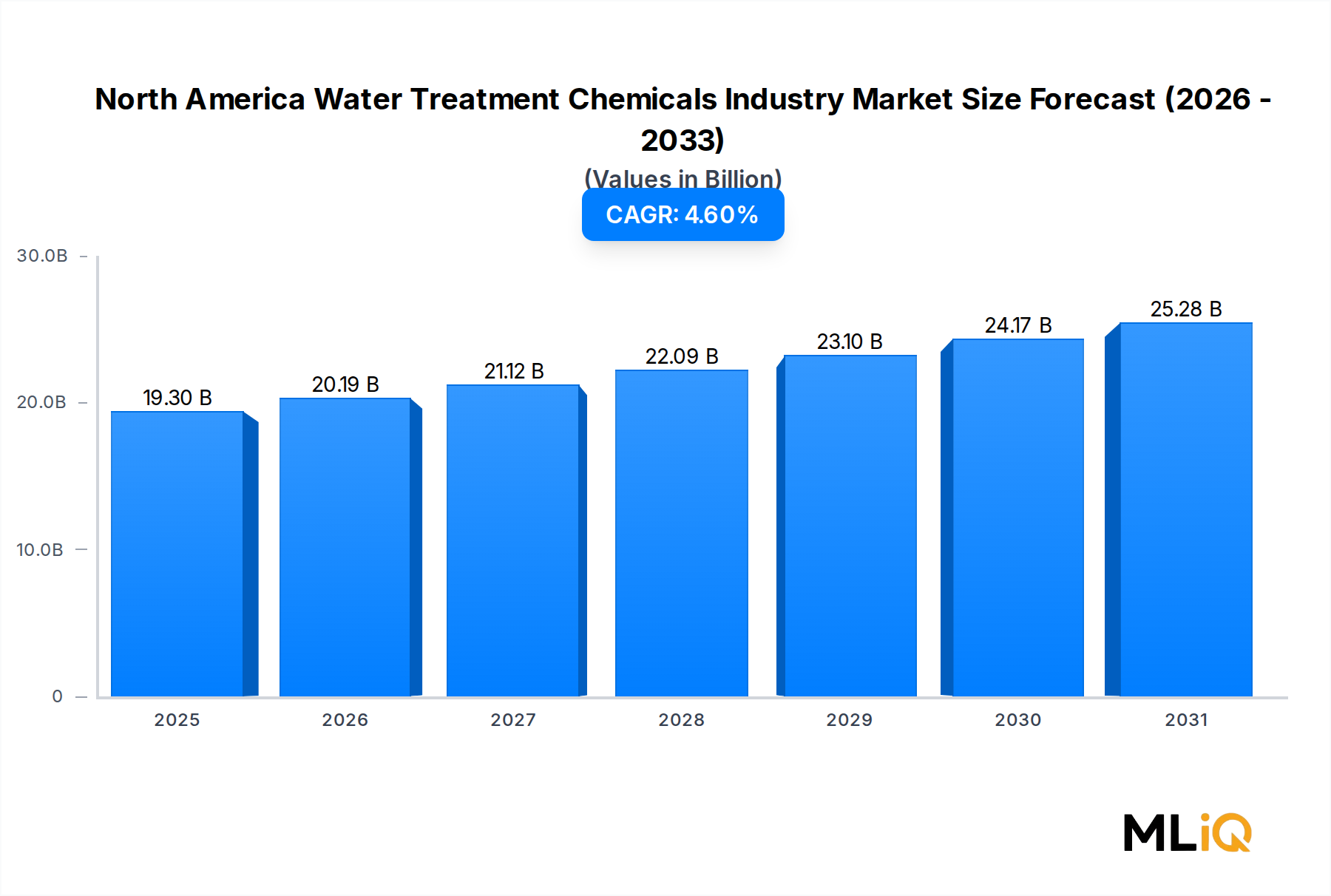

| 成長率 | 2020年から2034年までのCAGR 4.6% |

| セグメンテーション |

|

当社の厳格な調査手法は、多層的アプローチと包括的な品質保証を組み合わせ、すべての市場分析において正確性、精度、信頼性を確保します。

本「北米水処理薬品市場」調査レポートは、高精度かつ実行可能で包括的な市場インサイトを提供するべく設計された、堅牢で多角的な調査手法を採用しています。当社の調査アプローチは、厳密な分析フレームワークに裏打ちされた一次調査と二次調査の両方の経路を統合し、85~90%のデータ精度レベルを確保しています。すべての市場データおよび予測は、購入時点まで厳密に更新されており、最新の市場動向と業界の進展を反映しています。

| Stakeholder Role | Interview Share (%) |

|---|---|

| 水処理オペレーション責任者 | 35% |

| 調達担当副社長(薬品) | 30% |

| 製品ラインマネージャー(水処理薬品) | 20% |

| 環境コンプライアンスマネージャー | 15% |

| Company Type | Representation (%) |

|---|---|

| 水処理薬品メーカー | 30% |

| 産業エンドユーザー(電力、石油・ガス、食品・飲料) | 30% |

| 地方水道局 | 20% |

| 薬品販売業者 | 10% |

| 水処理薬品の原材料サプライヤー | 10% |

一次調査は、当社の市場分析の礎をなし、総調査努力の70~80%を占めています。この集中的な段階では、北米水処理薬品業界のバリューチェーン全体にわたる主要なステークホルダーとの直接的かつ詳細なエンゲージメントを含み、一次的な定性的および定量的データを収集します。当社の一次インタビューは、市場ドライバー、制約、機会、競争環境、技術的進歩、価格動向、規制影響に関する重要なインサイトを引き出すために、細心の注意を払って構造化されています。

インタビュー対象となった主要なステークホルダーは以下の通りです。

これらのインタビューは、市場にとって重要な多様な企業タイプにわたって行われました。

これらの専門家との協議から得られたインサイトは、二次調査の発見事項を検証し、新たなトレンドを特定し、公開情報源では入手困難な市場力学に関するニュアンスの取れた視点を得るために不可欠です。

一次調査を補完するものとして、二次調査は、残りの20~30%の調査努力を占めています。この段階では、さまざまな信頼できる公開および専有ソースからの広範なデータマイニングと分析が含まれ、市場に関する包括的な基礎的理解を確立します。当社の二次調査は、広範かつ深い視点を確保するために、数多くの信頼性の高いデータベースと出版物を活用しています。

利用された主要な二次ソースは以下の通りです。

二次データのこの包括的なレビューにより、市場規模の推定、歴史的トレンド、技術的進歩、競争環境分析、および規制フレームワークを確立することが可能になります。

当社の市場推定プロセスは、トップダウンアプローチとボトムアップアプローチの両方を統合し、多段階のデータトライアンギュレーションによって強化されており、予測の可能な限り最高の精度と信頼性を確保します。

ボトムアップアプローチは、可能な限り低いレベルでの需要の詳細な分析を含み、それらを集計して全体的な市場規模に到達します。北米水処理薬品市場の場合、これには以下が含まれます。

トップダウンアプローチは、北米のマクロ経済指標、産業支出、および全体的な産業生産量から導き出される広範な市場推定から始まり、それを特定の製品タイプ、エンドユーザー産業、および地域セグメントに分解します。

データトライアンギュレーションは、一次インタビュー、二次ソース、および当社の定量的モデルから得られた結果の相互参照と検証を含みます。この反復プロセスは、矛盾を特定し、調整するのに役立ち、市場数値の堅牢性と信頼性を向上させます。2026年から2034年までの期間の予測は、歴史的成長率、予測されるエンドユーザー産業の拡大、規制変更、技術的シフト、およびマクロ経済要因を組み込んだ高度な統計モデリング手法を使用して生成されます。

データ精度と品質の最高水準を維持することは最重要です。当社の厳格な品質保証プロセスにより、推定データ精度レベル85~90%が保証されます。すべてのデータポイント、市場推定、および予測は、複数の検証レイヤーを経ています。

さらに、最新の市場インテリジェンスを提供するという当社のコミットメントは、すべてのレポートが購入時点まで綿密に更新され、北米水処理薬品業界における最新の動向を反映していることを意味します。これにより、クライアントは戦略的意思決定のためのタイムリーで関連性の高い、高精度のインサイトを受け取ることができます。

BASF SE、コベストロAG、アルケマグループなどの主要プレーヤーは、進化する最終用途の需要に応えるため、バイオベースおよび水性コーティング製剤に投資しています。化学メーカーと繊維OEM間の戦略的パートナーシップは、製品の商品化期間を加速させています。クラリアントとソルベイも、医療および輸送用途をターゲットとした機能性コーティングのポートフォリオを拡大しています。

アジア太平洋地域が最も急速に成長しており、中国、インド、ASEAN諸国における繊維製造の急速な拡大に牽引され、推定42%の市場シェアを占めています。建設および輸送用途向けのコーティングされた技術繊維の国内消費の増加が主な促進要因です。特にインドは、世界のコーティングサプライヤーを惹きつける低コストの生産拠点として地位を確立しています。

ヨーロッパは、自動車、医療、保護服セグメントにおける高価値の用途に支えられ、世界市場の約26%を占めています。ドイツおよびベネルクス諸国を拠点とするメーカーが配合のベンチマークを設定しており、コベストロAGやタナテックス・ケミカルズB.V.などの企業がこの地域に本社を置いています。強力な研究開発インフラと厳格な性能基準が、他の地域と比較してプレミアム価格設定と高いユニットあたりの価値を推進しています。

熱可塑性樹脂セグメントは、そのリサイクル性、加工柔軟性、高性能繊維基材との適合性により、市場を支配すると予測されています。水性ポリウレタンおよびフッ素ポリマーフリーの配合は、PFASベースのコーティングの代替品として注目を集めています。SRFリミテッドおよびフォーミュレーテッド・ポリマー・プロダクツ社は、多機能繊維用途向けに高度な熱可塑性コンパウンド開発に投資している企業の一部です。

ヨーロッパのREACHや北米のEPAガイドラインなどの規制枠組みは、主要な制約として認識されており、溶剤ベースのコーティング生産者にとって再配合コストを増加させています。フッ素化合物および重金属ベースの仕上げに対する規制は、メーカーに準拠した水性およびバイオ由来システムへの移行を加速させています。コンプライアンスの負担は小規模な配合業者に不釣り合いに影響し、BASF SEやソルベイなどの大手プレーヤーへの市場シェアの統合を促進する可能性があります。

アジア太平洋諸国、特に中国とインドは、欧米の下流メーカーに完成コーティング生地や原ポリマーコーティング材料を供給する主要な輸出拠点として機能しています。ヨーロッパは、量産グレードのコーティング繊維の純輸入国である一方で、高仕様の配合物や特殊化学品を輸出しています。貿易の流れは、関税構造、炭素国境調整メカニズム、および地域的なサプライチェーンの多様化を促進するニアショアリングの傾向によってますます影響を受けています。