1. What are the major growth drivers for the Aircraft Navigation Lights Market market?

Factors such as are projected to boost the Aircraft Navigation Lights Market market expansion.

Aircraft Navigation Lights Market

Aircraft Navigation Lights Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

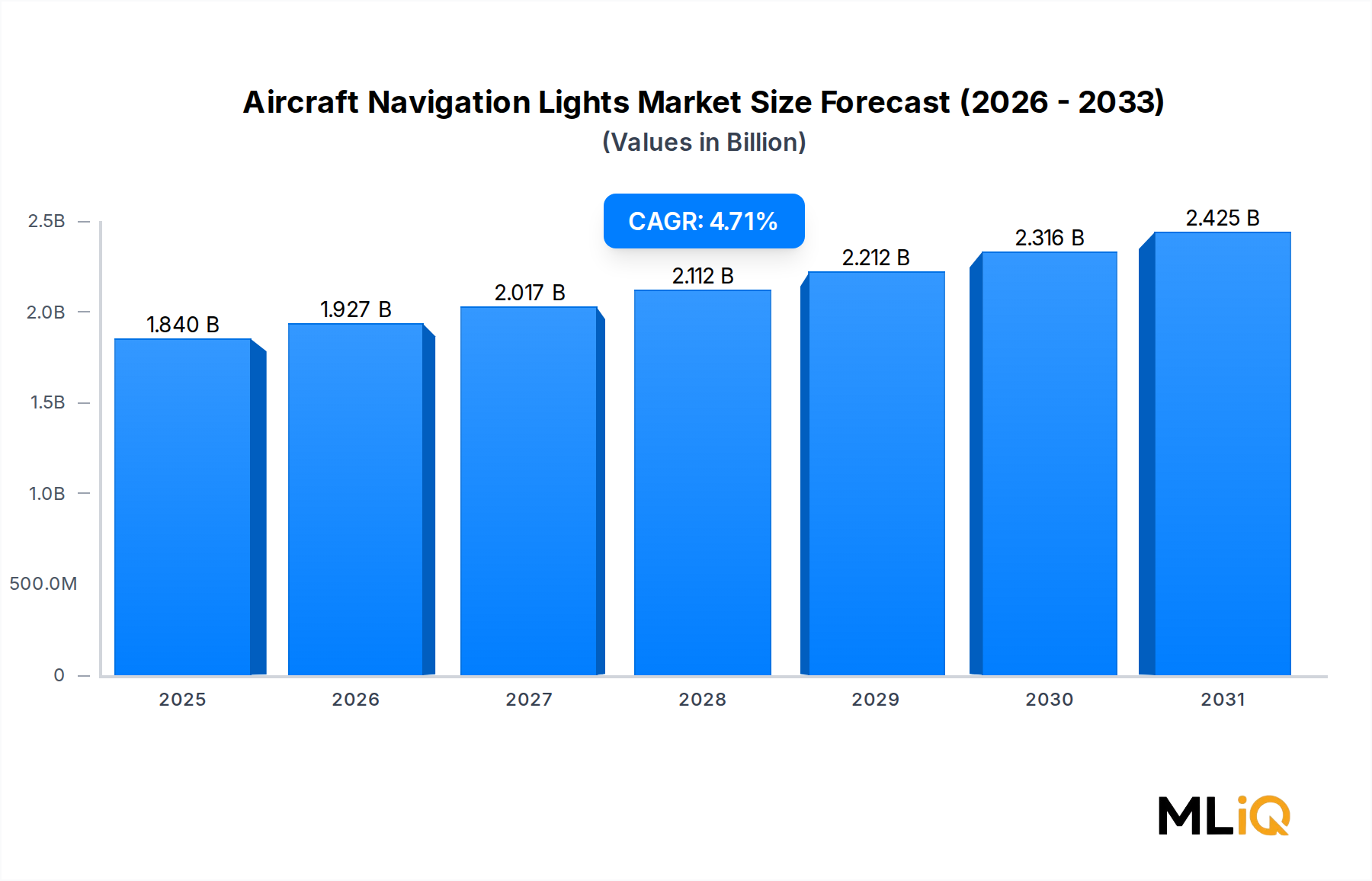

The global Aircraft Navigation Lights Market is valued at $1.84 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.71% through 2033, driven by a confluence of fleet modernization programs, rising air traffic volumes, and the accelerating shift toward energy-efficient lighting technologies. Navigation lights are a safety-critical component of every airworthy aircraft, mandated by international aviation authorities to signal an aircraft's position, heading, and status to other aircraft and ground personnel. Their continuous, non-discretionary demand profile insulates the market from cyclical aerospace downturns to a significant degree.

The primary macro tailwind sustaining this market is the unprecedented recovery and growth of global commercial aviation following the disruptions of the early 2020s. Airlines worldwide are accelerating fleet renewal cycles, placing large orders for next-generation narrowbody and widebody aircraft equipped from the outset with modern LED-based navigation lighting systems. The International Air Transport Association (IATA) projects that annual passenger numbers will surpass 4.7 billion by 2026, compelling carriers to expand operational fleets and, by extension, create sustained demand for both original equipment manufacturer (OEM) and aftermarket navigation lighting solutions.

On the technology side, the rapid displacement of legacy halogen and xenon lamp systems by LED technology is the single most transformative force reshaping product portfolios across the value chain. LED navigation lights offer service lives exceeding 50,000 hours compared to roughly 1,000–2,000 hours for incandescent equivalents, dramatically reducing maintenance intervals, lifecycle costs, and unscheduled aircraft-on-ground (AOG) events. This operational economics argument resonates equally with commercial operators seeking to minimize downtime and with military procurement agencies focused on reducing logistical burdens.

Military modernization programs in North America, Europe, and the Asia Pacific region represent a secondary but structurally important demand pillar. Defense budgets in NATO member states are being increased toward the 2% of GDP benchmark, with rotary-wing and fixed-wing platform upgrades incorporating advanced lighting suites that meet stringent night-vision imaging system (NVIS) compatibility requirements.

Looking forward through 2033, the market outlook is constructive. Emerging aviation markets in South and Southeast Asia, the Middle East, and Sub-Saharan Africa are expanding their domestic fleets, creating greenfield installation demand. Simultaneously, the growing urban air mobility (UAM) and advanced air mobility (AAM) sectors — encompassing electric vertical takeoff and landing (eVTOL) aircraft — are establishing new regulatory frameworks for navigation lighting that incumbent suppliers are actively working to address. The intersection of lightweight design requirements, low-power budgets, and high-reliability mandates in UAM platforms is expected to catalyze a new wave of product innovation, providing incremental revenue opportunities for agile participants in the Aircraft Navigation Lights Market.

Among all technology segments within the Aircraft Navigation Lights Market — LED lamps, halogen lamps, and xenon lamps — the LED lamp segment occupies the commanding revenue position and is extending its share lead with each successive product generation. As of 2025, LED navigation lights account for an estimated majority share of new aircraft installations globally, reflecting a structural and largely irreversible technology transition that began gaining momentum in the mid-2010s.

The dominance of LED lamps is rooted in a multi-dimensional value proposition that addresses the priorities of every major stakeholder in the aviation value chain. For airlines and aircraft operators, the operational cost advantage is decisive. LED navigation lights consume between 70% and 85% less electrical power than equivalent halogen assemblies, contributing measurably to fuel efficiency and reducing generator load on aircraft electrical systems. Given that fuel represents 20–30% of total airline operating costs, even marginal reductions in parasitic electrical consumption are financially meaningful when aggregated across large fleets operating thousands of cycles per year.

For maintenance, repair, and overhaul (MRO) organizations, the extended service life of LED units — routinely rated at 50,000 hours or more — translates directly into fewer scheduled replacement events, lower labor costs, and reduced spare parts inventory requirements. This has the secondary effect of shifting aftermarket revenue dynamics; while unit replacement frequency declines, the higher initial acquisition price of LED assemblies partially offsets this volume reduction, sustaining overall aftermarket revenue pools.

From an OEM integration standpoint, LED navigation lights offer design flexibility that is particularly valuable for next-generation aircraft programs. Their compact form factors enable aerodynamically optimized wingtip and fuselage installations, and their solid-state construction eliminates filament fragility concerns associated with vibration-intensive operating environments. Manufacturers of business jets, regional turboprops, and rotorcraft have embraced LED lighting as a standard fitment, further broadening the installed base.

Key players competing for leadership within the LED lamp segment include Astronics Corporation, which has invested substantially in proprietary LED optical designs optimized for FAA and EASA certification standards; Aveo Engineering Group, recognized for its compact, multi-function LED navigation and anti-collision light assemblies targeting general aviation and business aviation platforms; and STG Aerospace Limited, which has brought significant LED cabin and exterior lighting expertise to the navigation lighting domain. Honeywell International Inc. leverages its broad aerospace systems integration capabilities to offer LED navigation lighting as part of integrated exterior lighting packages for commercial transport category aircraft.

The LED segment's share is not merely growing — it is consolidating at the expense of both halogen and xenon alternatives. Xenon lamp systems, once favored for their high-intensity strobe output, are being displaced by high-power LED strobe solutions that replicate photometric performance while offering vastly superior reliability and power efficiency. Halogen lamps retain a residual presence in older legacy fleets and cost-sensitive general aviation applications, but aircraft retirement rates and the availability of retrofit LED upgrade kits are steadily eroding even this segment. Regulatory tailwinds, including advisory circulars from the FAA encouraging LED adoption for its safety and reliability benefits, reinforce the LED segment's trajectory toward near-total market dominance by the early 2030s.

The competitive intensity within the LED navigation lights sub-segment is high, with participants differentiating on the basis of photometric performance (candela output, beam angle precision), NVIS compatibility for military applications, environmental sealing ratings (IP67/IP68), weight reduction through advanced thermal management, and the breadth of supplemental type certificate (STC) coverage enabling retrofit installations on in-service aircraft types. Companies that can offer broad STC portfolios and streamlined certification pathways hold a meaningful competitive advantage, particularly in the aftermarket channel where rapid return-to-service is a paramount customer requirement.

Several quantifiable drivers and a set of identifiable constraints govern the growth trajectory of the Aircraft Navigation Lights Market through the forecast horizon.

Primary Driver — Fleet Expansion and Renewal: Airbus and Boeing collectively hold order backlogs exceeding 14,000 commercial aircraft as of early 2025, representing multiple years of production at current build rates. Each new aircraft delivery incorporates a full complement of navigation lights, generating a structural demand floor that is largely insensitive to short-term traffic fluctuations. The widening adoption of eVTOL platforms, with over 700 electric air taxi designs in various stages of development globally, introduces an entirely new aircraft category requiring navigation lighting certification, adding incremental upside.

Secondary Driver — Military Modernization: Defense budgets in the United States, United Kingdom, Germany, and India have been raised in real terms between 2022 and 2025, funding procurement of advanced fighter aircraft, tankers, maritime patrol aircraft, and rotorcraft. Each platform requires specialized navigation lighting, including NVIS-compatible systems that prevent interference with night-vision equipment during tactical operations. The U.S. Department of Defense alone accounts for the acquisition or modification of several hundred aircraft annually.

Tertiary Driver — Retrofit and Aftermarket Activity: The global in-service commercial fleet exceeds 28,000 aircraft, the majority of which still operate legacy halogen or older LED lighting systems. Regulatory guidance from the FAA (Advisory Circular AC 20-30B) and EASA Part-21 subpart E framework supports STC-based retrofit programs, enabling operators to upgrade to current-generation LED systems. This retrofit wave is estimated to represent a multi-hundred-million-dollar annual opportunity.

Primary Constraint — Supply Chain and Component Shortages: Semiconductor availability constraints, which emerged acutely in 2021–2022 and persist in more moderate form through 2025, have affected LED driver electronics and microcontroller components embedded in modern navigation light assemblies. Lead times for certain specialized optoelectronic components have extended to 26–52 weeks, constraining manufacturers' ability to fulfill OEM and aftermarket orders at pace.

Secondary Constraint — Certification Complexity and Cost: Obtaining FAA and EASA airworthiness approval for new navigation light designs involves extensive photometric testing, environmental qualification (RTCA DO-160G), and electromagnetic compatibility assessment. Total certification costs for a new product family can reach $2–5 million, creating a meaningful barrier to entry and slowing the time-to-market for innovative designs from smaller participants.

The competitive landscape of the Aircraft Navigation Lights Market is moderately consolidated, with a mix of large diversified aerospace suppliers, specialized lighting technology companies, and niche innovators.

B/E Aerospace Inc.: A major aerospace interior and exterior systems supplier, B/E Aerospace has leveraged its strong OEM relationships with Airbus and Boeing to supply integrated exterior lighting solutions including navigation light assemblies for commercial transport aircraft.

Honeywell International Inc.: Honeywell brings deep systems integration expertise and global aftermarket reach to the navigation lighting segment, offering LED-based navigation and anti-collision light products as part of broader avionics and electrical systems packages for commercial and business aviation customers.

Diehl Stiftung & Co. KG: The German aerospace and defense conglomerate Diehl has established a strong position in aircraft cabin and exterior lighting through its Diehl Aerospace subsidiary, supplying navigation lighting systems to Airbus program lines and European defense customers.

Astronics Corporation: Astronics is a focused aerospace lighting and electronics specialist with significant proprietary LED navigation and anti-collision lighting product portfolios, supported by a broad STC database enabling retrofit sales across hundreds of aircraft types.

UTC Aerospace Systems: As part of the Raytheon Technologies (now RTX Corporation) family, UTC Aerospace Systems supplies exterior lighting systems including navigation lights for military and commercial platforms, leveraging deep defense program relationships.

Zodiac Aerospace: Now integrated within Safran Cabin, Zodiac Aerospace historically contributed exterior lighting capabilities to narrowbody and widebody OEM programs, with its product intellectual property absorbed into Safran's aerospace electrical systems portfolio.

Aveo Engineering Group: A specialized aviation lighting innovator, Aveo Engineering Group has built a strong reputation in the general aviation, business aviation, and rotorcraft segments for compact, high-performance LED navigation and strobe light assemblies with broad STC coverage.

Bruce Aerospace: Bruce Aerospace focuses on FAA-certified LED exterior lighting products, including navigation lights and strobe systems, targeting both OEM installations and the large general aviation retrofit market with competitively priced solutions.

Cobham plc: Cobham's aerospace and defense systems division has supplied lighting and electrical systems to military aircraft programs globally, with particular strength in UK Ministry of Defence platform programs and NATO allied force aviation.

STG Aerospace Limited: STG Aerospace is recognized for innovation in aircraft lighting, having pioneered photoluminescent cabin emergency lighting and extending its expertise into LED exterior navigation lighting solutions for commercial and regional aircraft operators.

January 2024: Astronics Corporation announced the expansion of its LED navigation light STC portfolio to cover an additional 47 Boeing 737 Classic and Next-Generation variants, broadening retrofit market access for operators transitioning away from legacy halogen systems.

March 2024: The European Union Aviation Safety Agency (EASA) published updated guidance material under CS-25 Amendment 28 clarifying photometric performance requirements for LED-based navigation lights on large transport category aircraft, providing regulatory certainty for next-generation product development programs.

June 2024: Aveo Engineering Group received FAA production approval for its new FoxFire ULTRA series LED navigation and anti-collision light system, designed for rotorcraft and light sport aircraft applications with a weight reduction of 35% versus the prior generation.

September 2024: Honeywell International Inc. and a leading narrowbody aircraft lessor announced a fleet-wide LED navigation light retrofit program covering 180 aircraft, representing one of the largest single aftermarket LED conversion contracts recorded in the year.

November 2024: STG Aerospace Limited entered a memorandum of understanding with an Asia Pacific regional airline to supply LED exterior lighting packages, including navigation lights, for a fleet of 60 ATR 72 turboprop aircraft, marking a significant expansion of the company's presence in the Asia Pacific aftermarket.

February 2025: The FAA issued an airworthiness directive referencing accelerated inspection requirements for a specific legacy halogen navigation light assembly model installed on certain business jet types, indirectly accelerating operator decisions to transition to certified LED replacement units.

April 2025: Diehl Stiftung & Co. KG announced a long-term supply agreement with Airbus to provide LED exterior lighting systems, including navigation lights, for the A320neo family production line through 2030, securing a significant portion of the company's forward order book.

The Aircraft Navigation Lights Market exhibits distinct regional demand profiles shaped by fleet composition, regulatory environment, defense spending, and the pace of commercial aviation expansion.

North America: North America represents the single largest regional market, accounting for an estimated 34–36% of global revenue in 2025. The United States drives this position through its combination of the world's largest commercial airline fleet, an active general aviation community of approximately 220,000 registered aircraft, and substantial military aviation procurement. The U.S. aftermarket is particularly robust, with FAA STC-enabled LED retrofit programs generating consistent demand. The regional CAGR is projected at approximately 4.2% through 2033, reflecting a mature market with stable replacement cycles and incremental growth from military modernization programs.

Europe: Europe is the second-largest regional market, with estimated revenue share of 25–27% in 2025. The region is characterized by strong OEM demand anchored to Airbus production programs in France, Germany, and the United Kingdom, alongside active MRO networks servicing both intra-European and long-haul carriers. EASA's progressive regulatory framework actively supports LED adoption. The European CAGR is estimated at 4.4%, slightly above North America, driven by ongoing fleet renewal and the integration of Zodiac/Safran and Diehl supply chains into next-generation Airbus programs.

Asia Pacific: Asia Pacific is identified as the fastest-growing regional market, with a projected CAGR of 5.8–6.2% through 2033. China and India are the primary growth engines, with both nations executing ambitious domestic aviation expansion programs. China's COMAC C919 and ARJ21 programs generate indigenous OEM demand, while India's airline sector — expanding at among the fastest rates globally — drives fleet additions requiring both OEM and aftermarket lighting supply. Japan, South Korea, and the ASEAN bloc contribute incremental demand from established carriers and growing low-cost carrier fleets.

Middle East & Africa: This region is experiencing above-average growth, estimated at a CAGR of 5.0–5.3%, driven by the continued expansion of Gulf Carrier fleets and increasing defense aviation investment from GCC member states. Infrastructure investment in airport ground lighting systems, a related demand segment, is also supporting regional market activity.

South America: South America represents the smallest regional share at approximately 4–5% of global revenue, with a moderate CAGR of 3.5–3.8%. Brazil, anchored by Embraer OEM activity and the LATAM Airlines Group fleet, is the primary demand center, though economic volatility has historically moderated aftermarket investment cycles.

The supply chain for the Aircraft Navigation Lights Market is moderately complex, integrating upstream materials, electronic components, optical systems,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.71% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Aircraft Navigation Lights Market market expansion.

Key companies in the market include B/E Aerospace Inc., Honeywell International Inc., Diehl Stiftung & Co. KG, Astronics Corporation., UTC Aerospace Systems, Zodiac Aerospace, Aveo Engineering Group, Bruce Aerospace, Cobham plc, STG Aerospace Limited.

The market segments include Type, Application, Fit, End-User.

The market size is estimated to be USD 1.84 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Aircraft Navigation Lights Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aircraft Navigation Lights Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.