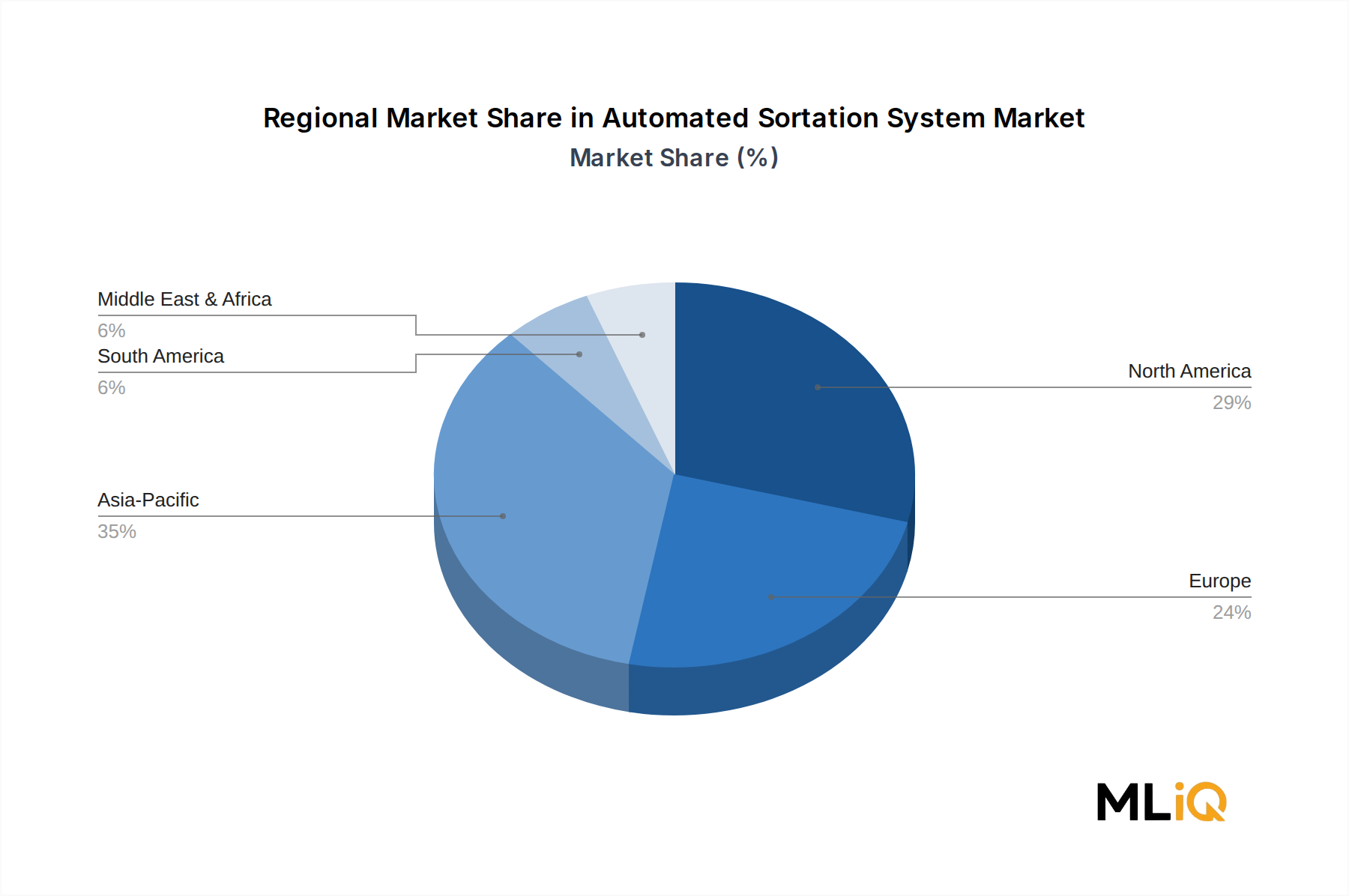

The Automated Sortation System Market exhibits pronounced regional differentiation in terms of maturity, growth velocity, and primary demand drivers, with each major geography presenting distinct investment dynamics.

North America represents the most mature and revenue-dominant regional market, accounting for an estimated 35–38% of global revenue. The United States is the principal contributor, with large-scale deployments concentrated among major retail chains, 3PL operators, and postal service networks undergoing capacity modernization. The region's CAGR is estimated at approximately 8.5% through 2033, reflecting a market in the transition from initial automation adoption to system refresh and capacity expansion cycles. Canada and Mexico are secondary contributors, with Mexico emerging as a manufacturing and nearshoring hub that is generating incremental demand for industrial sortation in automotive and consumer goods supply chains.

Europe is the second-largest regional market, representing approximately 28–30% of global revenue. Germany, the United Kingdom, and France are the dominant national markets, driven by regulatory labor market dynamics, strong e-commerce penetration, and the geographic complexity of pan-European fulfillment networks. The region's estimated CAGR of 9.1% through 2033 reflects continued investment in sortation capacity upgrades driven by sustainability mandates that favor automated energy-efficient systems over manual operations. The Nordics and Benelux sub-regions are notable innovation centers for sortation technology integration.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 13.5–14% through 2033, reflecting China's dominant e-commerce ecosystem, India's logistics modernization initiative, Japan's chronic labor shortage environment, and Southeast Asia's rapidly expanding organized logistics infrastructure. China alone accounts for the majority of the regional market, with domestic champions and global vendors competing intensely for project awards tied to new fulfillment center construction.

Middle East and Africa represent an emerging growth frontier, with GCC countries — particularly the UAE and Saudi Arabia — investing in airport cargo sortation, postal automation, and modern trade distribution infrastructure as part of economic diversification programs. The regional CAGR is estimated at 11.2%, with growth concentrated in the GCC and South Africa.

South America is a nascent market with a CAGR of approximately 8.0%, driven primarily by Brazil's expanding e-commerce sector and Argentina's gradual infrastructure modernization, though macroeconomic volatility constrains capital deployment velocity.