Connectivity Segment Dominance in the MEA Inflight Entertainment and Connectivity Market

Within the MEA Inflight Entertainment and Connectivity Market, the connectivity sub-segment has emerged as the single largest and fastest-growing product type by revenue contribution, eclipsing traditional hardware and content segments in terms of investment priority and strategic airline focus. This dominance is not merely a transitional phenomenon but reflects a structural shift in how airlines, passengers, and technology vendors perceive value creation at 35,000 feet.

The connectivity segment encompasses all airborne broadband solutions, including satellite-based systems (Ku-band, Ka-band, and emerging LEO constellations), Air-to-Ground (ATG) networks, and hybrid connectivity architectures. The MEA region's geographic position — spanning vast oceanic and desert routes where terrestrial infrastructure is absent — makes satellite connectivity the default and dominant technology paradigm. High-throughput satellite (HTS) systems have dramatically reduced per-megabit costs, enabling airlines to deploy connectivity solutions that were economically unviable just five years ago.

Key players anchoring the connectivity segment in the MEA Inflight Entertainment and Connectivity Market include Inmarsat Global Limited, ViaSat Inc, Panasonic Corporation, and Honeywell International Inc. Inmarsat's GX Aviation service, operating on Ka-band HTS infrastructure, has achieved widespread adoption among Middle Eastern carriers, offering consistent speeds above 50 Mbps per aircraft. ViaSat's competing high-capacity satellite network provides strong coverage across North African and GCC routes. Panasonic's eXConnect platform integrates seamlessly with its in-seat entertainment architecture, creating a unified IFEC ecosystem that appeals to full-service carriers seeking vendor consolidation.

The growth dynamics within the connectivity sub-segment are being further catalyzed by the entry of LEO satellite operators. Constellations operating at altitudes below 1,200 kilometers offer latency profiles approaching 20–40 milliseconds, compared to 600+ milliseconds for traditional geostationary satellite systems. This latency reduction unlocks use cases previously impossible onboard aircraft, including real-time video conferencing, cloud gaming, and low-latency financial transactions — all of which are increasingly demanded by the business-class traveler segment prevalent on Middle Eastern long-haul routes.

Airlines are also evolving their commercial models around connectivity. Rather than charging passengers per-flight fees, carriers are migrating toward monthly subscription models, roaming agreements with mobile network operators, and freemium tiers supported by advertising revenue. This model shift is increasing connectivity take-up rates while stabilizing revenue streams for IFEC vendors. Emirates, Etihad, and Qatar Airways have been particularly aggressive in deploying premium connectivity offerings as a brand differentiator, and several African carriers are now following suit with support from multilateral development finance.

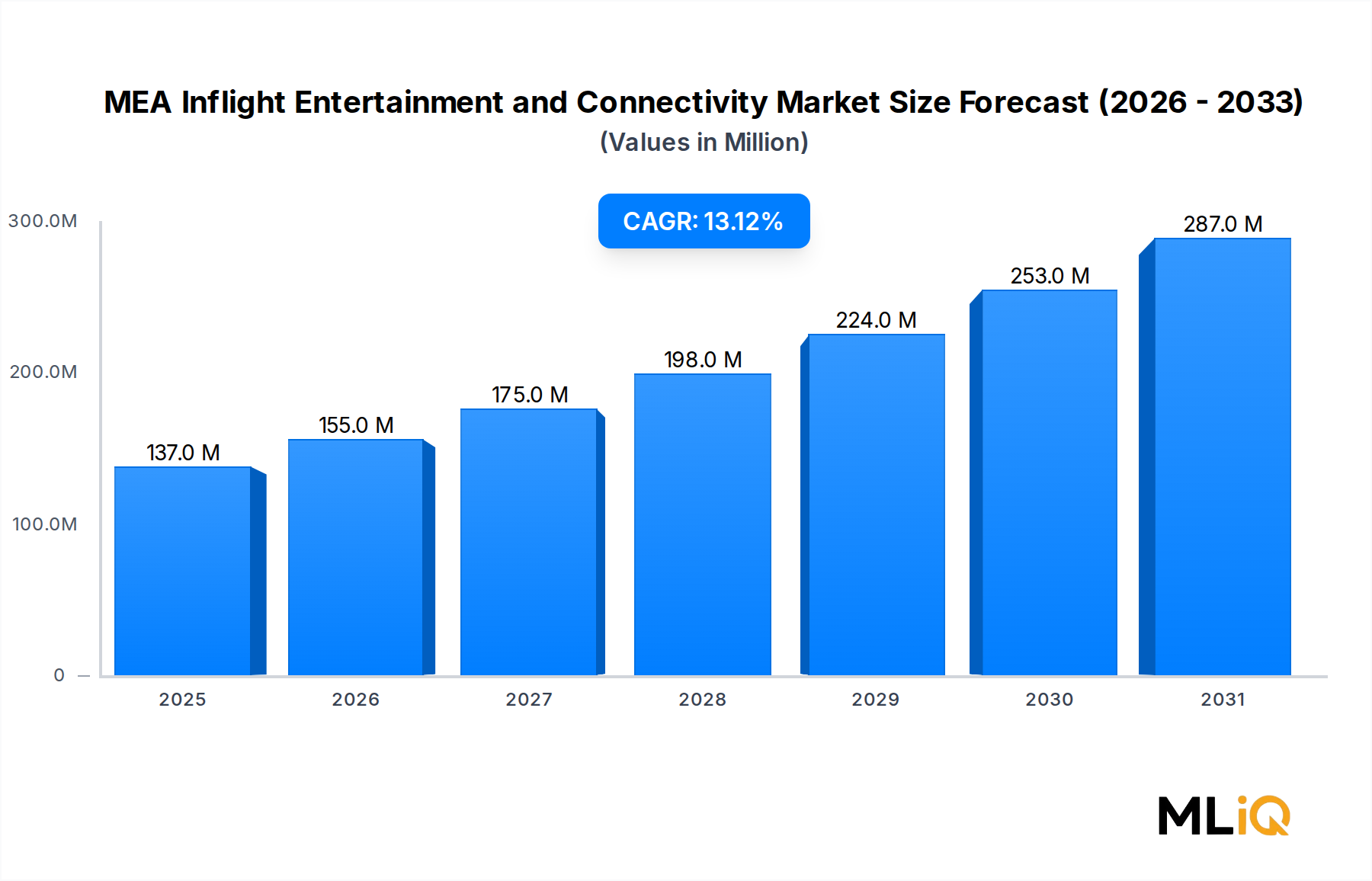

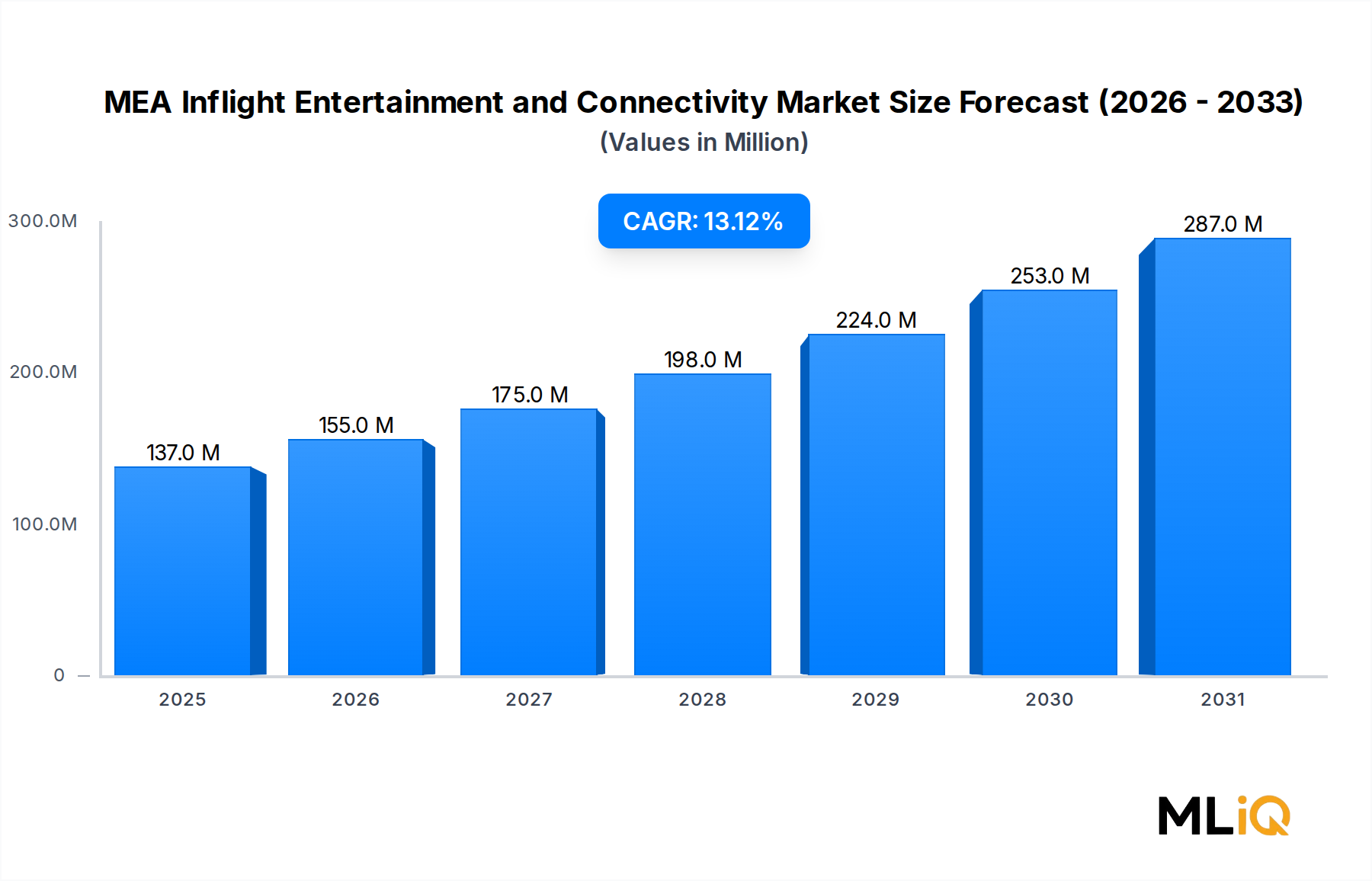

The share of the connectivity segment within the overall MEA Inflight Entertainment and Connectivity Market is estimated to be consolidating above 45% of total market revenue by 2025, with projections indicating this share will approach 55–58% by 2033 as hardware and basic content revenues face commoditization pressures. Retrofit programs targeting narrowbody fleets operating intra-GCC and Africa-Europe routes represent a significant untapped opportunity, with thousands of aircraft-tail units addressable in the medium term.

Vendor competition within this segment is intensifying. Thales Group's FlytLIVE Ka-band solution and Gogo Inc's business aviation connectivity platforms are expanding their commercial aviation footprints in the region. Meanwhile, Safran SA is leveraging its strong MRO network in Africa to offer connectivity upgrade packages bundled with cabin refurbishment services, lowering the adoption barrier for smaller African carriers with constrained capital budgets.