Commercial Aviation Dominance in the Aircraft Tugs Market

The commercial aviation segment represents the single largest end-use category within the Aircraft Tugs Market, accounting for an estimated 58–62% of total global revenue in 2025. This dominance is structural rather than cyclical, rooted in the sheer scale and density of commercial airline ground handling operations relative to military and general aviation segments.

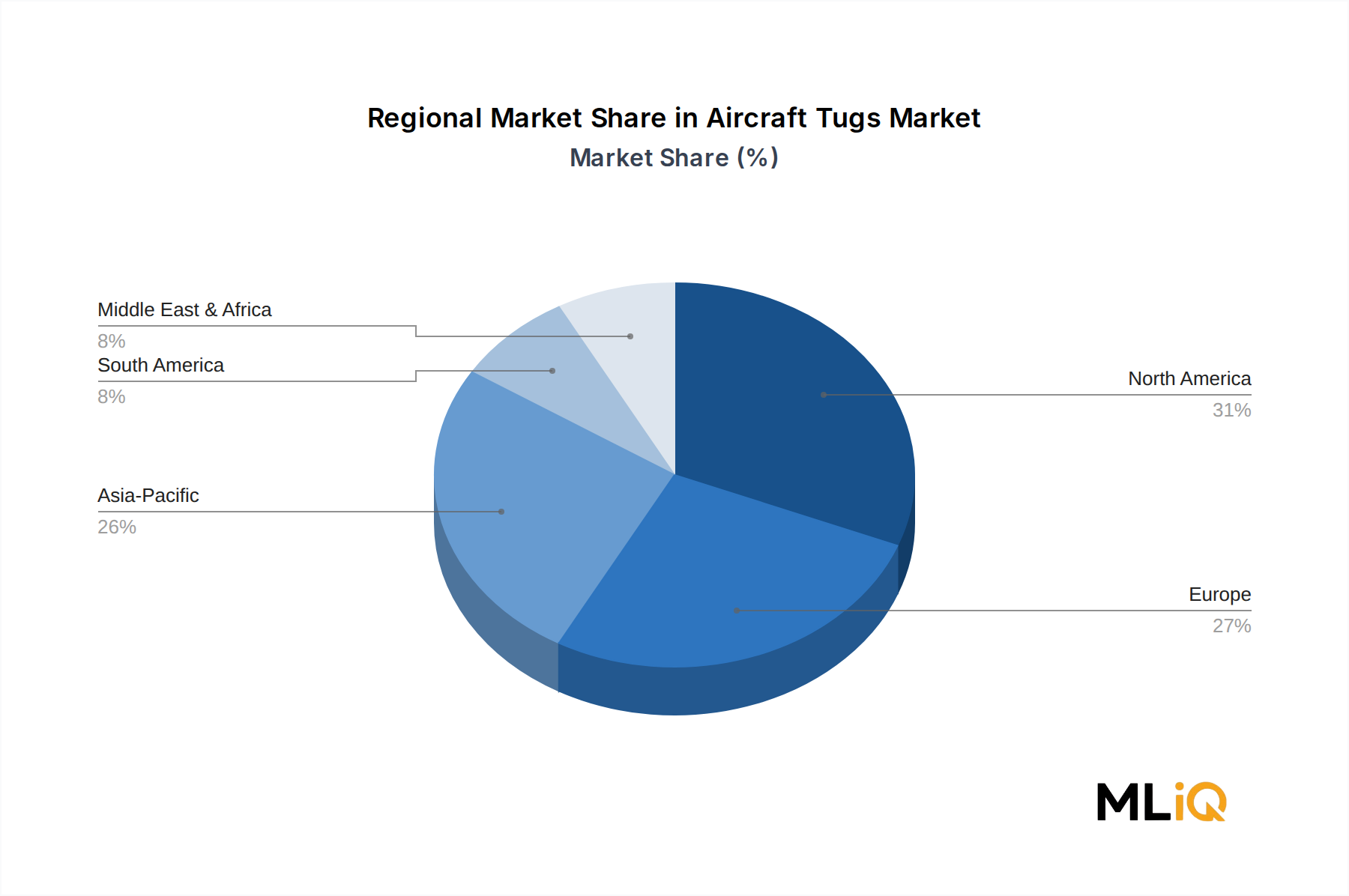

Commercial airports process tens of thousands of aircraft movements daily across their combined global network. Each movement typically requires at least one pushback or tow operation, meaning that high-frequency hub airports generate extraordinary utilization cycles for aircraft tug fleets. Major international gateway airports such as Hartsfield-Jackson Atlanta, Dubai International, London Heathrow, and Beijing Capital collectively handle hundreds of millions of passengers per year, translating into immense and sustained tug deployment density.

Within the commercial aviation segment, widebody aircraft handling represents the highest-value sub-category. Tugs designed to move aircraft in the Airbus A380, Boeing 747-8, and Boeing 777X class must deliver significantly higher tractive effort — often exceeding 100,000 lbf — and are correspondingly priced at a substantial premium over narrowbody-class equipment. The ongoing delivery of Boeing 777X aircraft and the continued operation of large Airbus A350 and Boeing 787 fleets ensure sustained demand for heavy-duty commercial tugs.

The low-cost carrier (LCC) expansion across Asia Pacific and Latin America is another key demand vector within this segment. LCCs typically operate high-frequency, short-turnaround narrowbody fleets, imposing intensive utilization demands on ground support equipment. Airlines such as IndiGo, AirAsia, and Ryanair operate among the largest single-type fleets in the world, and their ground handling partners must maintain correspondingly large and reliable tug inventories.

Towbarless tug adoption is accelerating fastest within the commercial segment, particularly among airlines and ground handlers seeking to reduce nose gear stress, eliminate towbar logistics, and improve pushback cycle times. Towbarless systems allow direct coupling to the aircraft nose gear, offering operational flexibility and enabling a single tug model to service multiple aircraft types. This versatility is especially valued by third-party ground handling companies managing mixed fleets across multiple airline customers.

Key players commanding significant share in the commercial aviation tug segment include TLD Group SAS, which offers a comprehensive portfolio spanning electric, diesel, and hybrid tugs across the full weight class spectrum. JBT Corporation holds a strong position through its legacy in airport equipment integration, offering both towbar and towbarless solutions. TREPEL Aircraft Equipment GmbH is particularly recognized for its high-capacity Challenger series towbarless tugs deployed across European major airports. Mototok International GmbH has gained notable market share with its remote-controlled, fully electric compact tug systems, which are increasingly specified by airlines seeking to minimize ramp crew requirements.

The commercial aviation segment's share is expected to remain stable in the 58–60% range through 2033, with modest share erosion possible if military modernization and UAV support infrastructure programs accelerate faster than currently projected. However, given the confirmed commercial aircraft orderbook depth and the ongoing global airport expansion pipeline, this segment will remain the primary revenue engine of the Aircraft Tugs Market for the foreseeable forecast horizon.