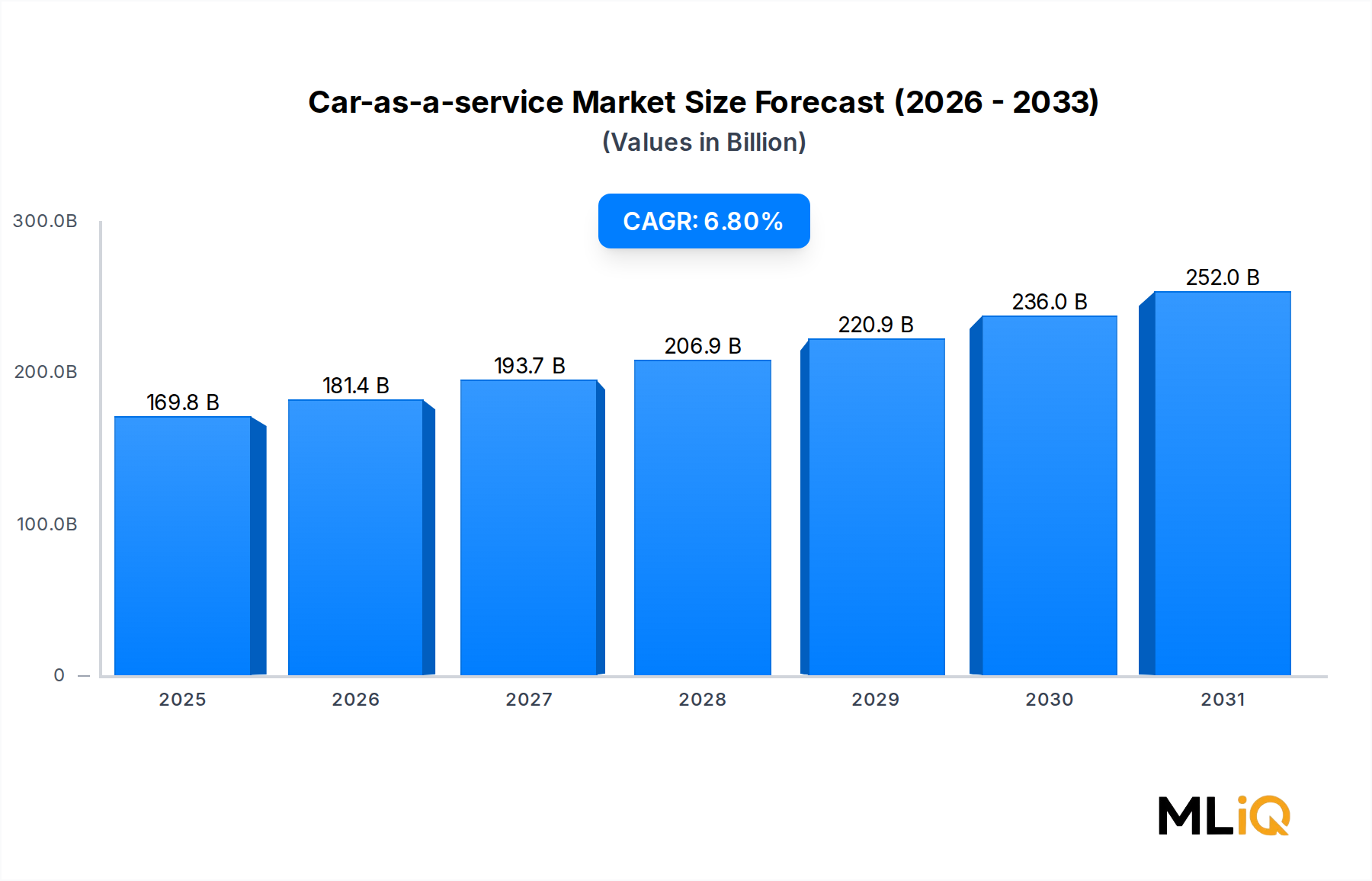

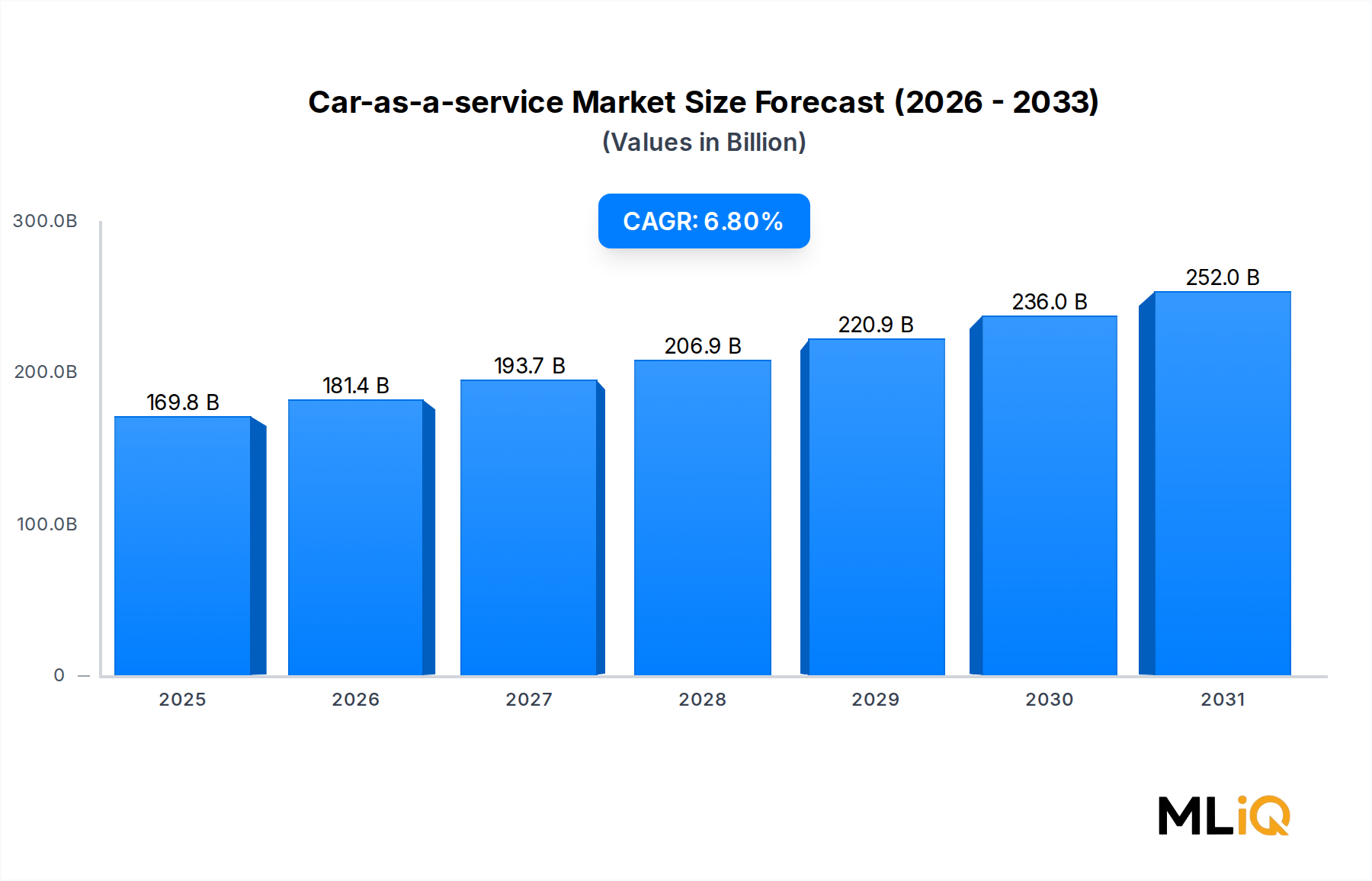

The global Car-as-a-service Market is positioned for sustained expansion over the forecast period 2025–2033, driven by shifting consumer preferences, urbanization trends, and the rapid digitization of transportation ecosystems. As of the base assessment year, the market is valued at $169.82 billion, reflecting the maturation of subscription-based and on-demand mobility models that are displacing traditional vehicle ownership paradigms across developed and emerging economies alike.

Projected growth at a compound annual growth rate (CAGR) of 6.8% through 2033 indicates that the market will generate substantial incremental revenue, compounding the existing base into a significantly larger addressable opportunity. This trajectory is underpinned by several macro-level tailwinds: rising urban congestion, increasing total cost of vehicle ownership, environmental mandates restricting internal combustion engine penetration in major cities, and the proliferation of smartphone-enabled mobility platforms that reduce friction in vehicle access.

Demand-side dynamics are equally compelling. The corporate end-use segment is progressively substituting traditional company-car fleet procurement with flexible CaaS arrangements that reduce capital expenditure and align vehicle costs with actual utilization. Simultaneously, the private consumer segment—particularly millennials and Gen Z cohorts in Tier-1 urban centers—increasingly favors access over ownership, fueling subscription and pay-per-use model adoption.

On the technology front, connectivity infrastructure, AI-driven fleet optimization, and embedded telematics are enabling operators to offer differentiated value propositions including real-time vehicle health monitoring, dynamic pricing, and seamless handoff between short- and long-term mobility contracts. These innovations are critical to margin improvement as operators scale.

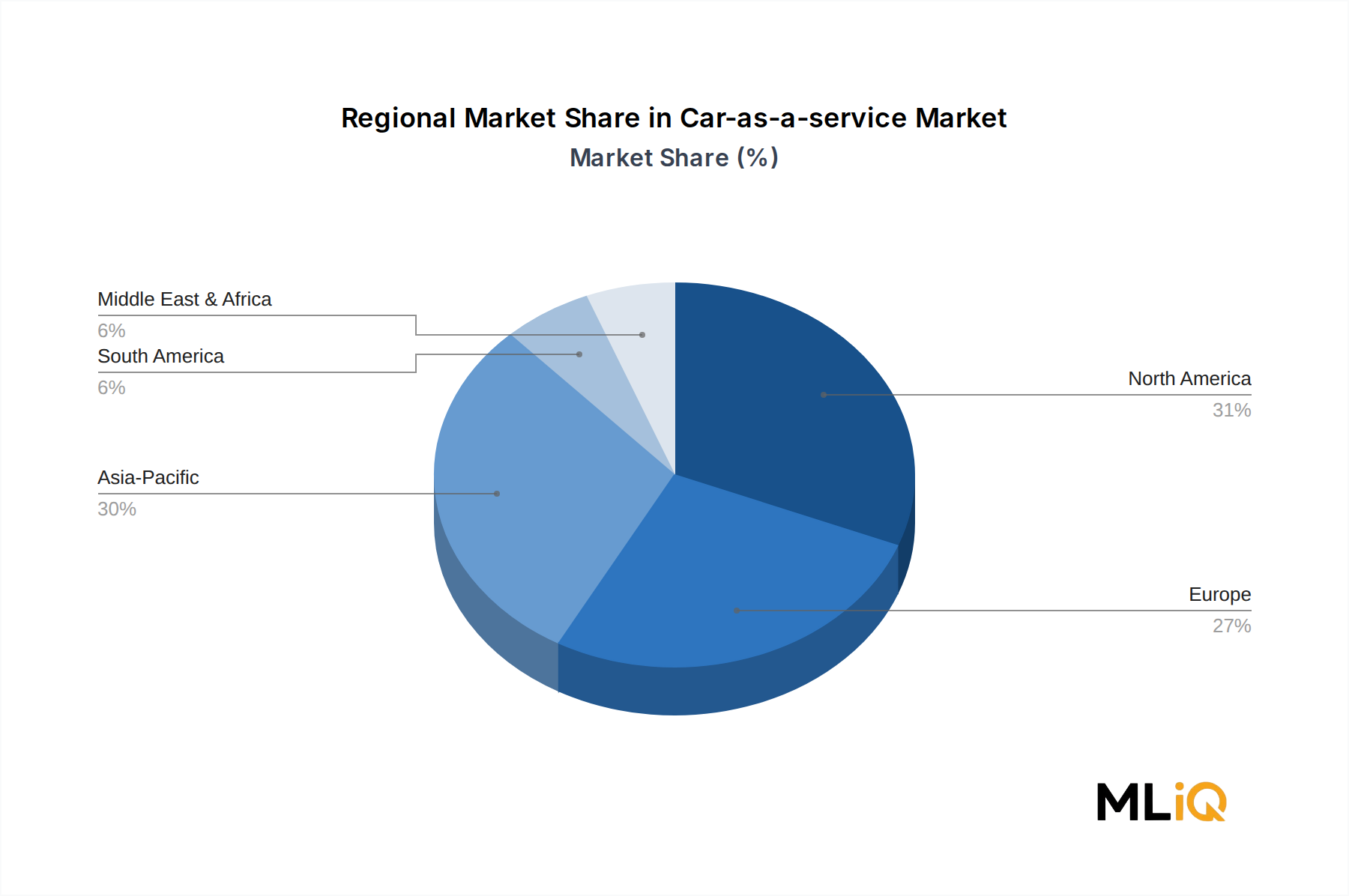

Geographically, Asia Pacific commands the fastest-growing demand trajectory, with China and India leading volume expansion due to favorable demographic profiles and aggressive EV infrastructure investments. North America and Europe remain the highest-revenue regions, with regulatory pressure—particularly in the European Union—catalyzing rapid fleet electrification within CaaS portfolios.

Key competitive dynamics include consolidation among platform providers, strategic OEM-to-service-provider pivots from companies such as Daimler AG, Volvo Car Corporation, and BMW Group, and the entry of fintech-enabled players such as Fair Financial Corp. offering flexible ownership alternatives. The competitive landscape is further complicated by the convergence of CaaS with adjacent markets including the Ride Hailing Market and the Vehicle Subscription Market, blurring traditional segment boundaries and intensifying pricing competition.

Looking forward through 2033, the market's growth narrative will be shaped by the pace of electric vehicle adoption within service fleets, the resolution of supply chain constraints affecting semiconductor and battery inputs, and the regulatory evolution of data monetization frameworks that govern connected mobility services.