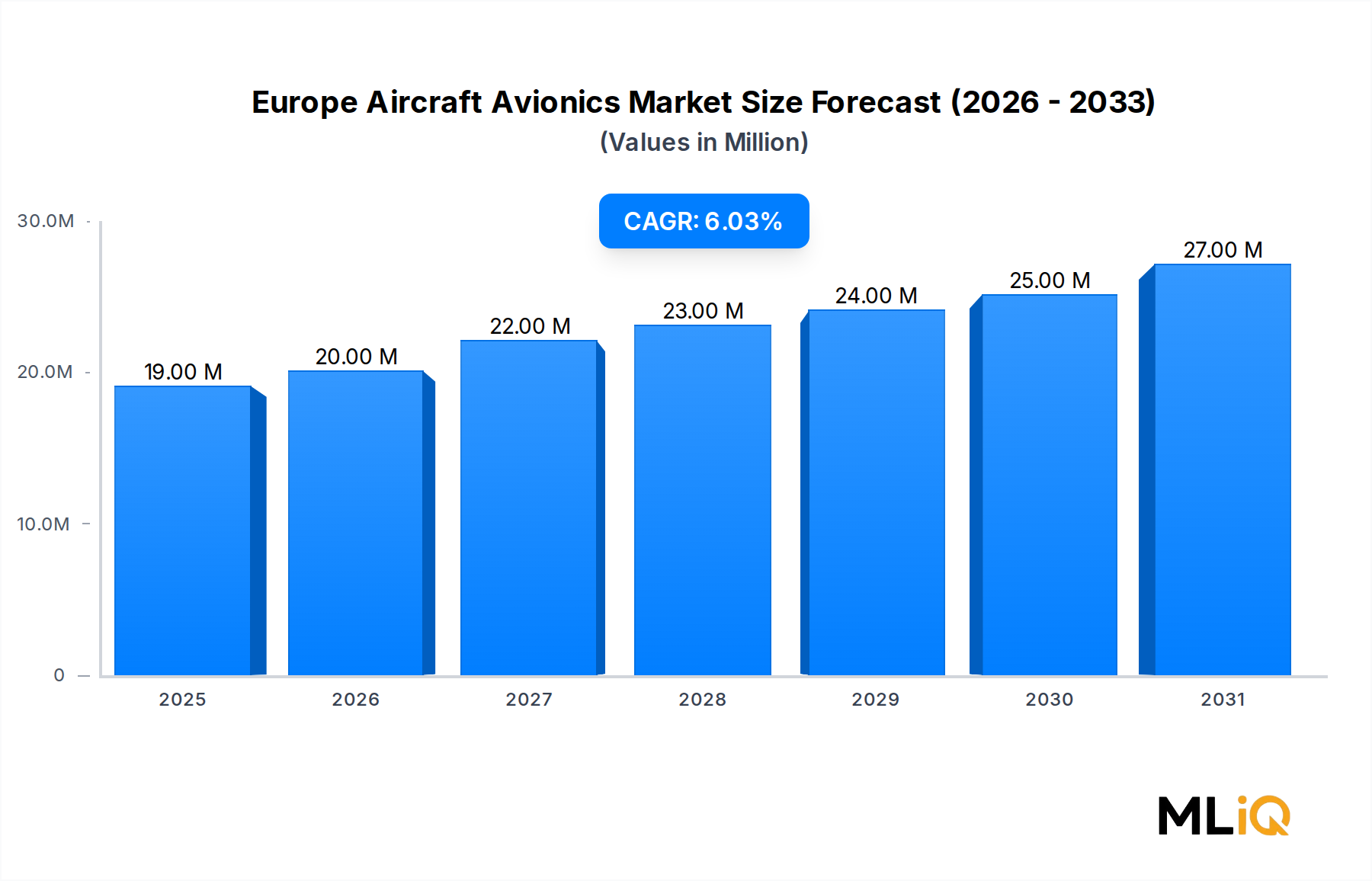

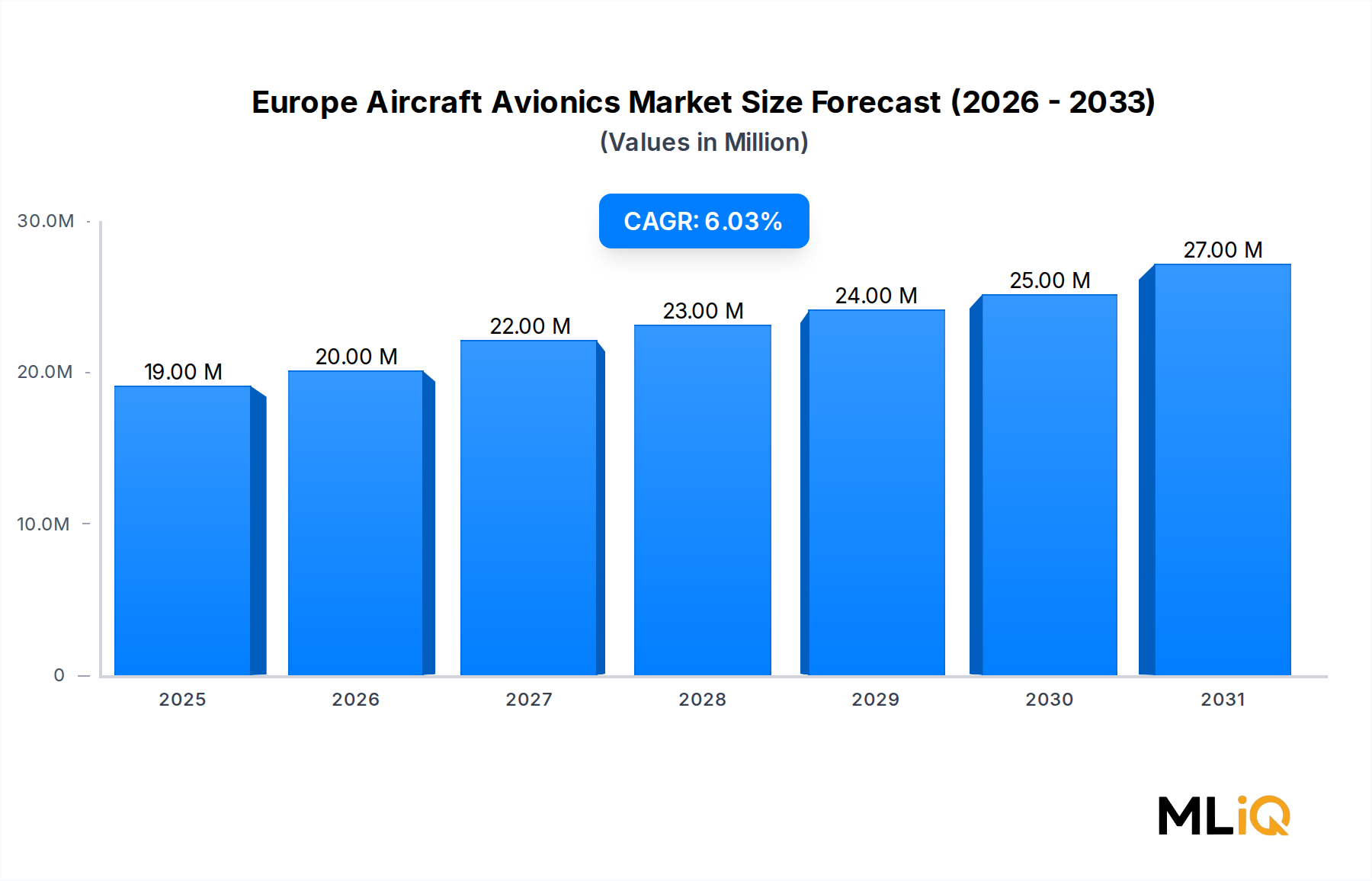

Commercial Aircraft Dominance in the Europe Aircraft Avionics Market

The commercial aircraft segment stands as the largest revenue-generating application within the Europe Aircraft Avionics Market, accounting for the highest share of total market value across the forecast period. This dominance is structural rather than cyclical, rooted in the sheer volume of commercial airframes operating across European airspace, the mandatory nature of avionics upgrade programs driven by regulatory compliance, and the sustained recovery of European air travel demand following the disruptions of 2020–2021.

Europe's commercial aviation ecosystem is anchored by a network of major flag carriers, low-cost carriers, and regional operators collectively operating thousands of aircraft. Airlines such as Lufthansa, Air France-KLM, Ryanair, and IAG-affiliated carriers represent an enormous installed base requiring continuous avionics maintenance, retrofits, and new-build equipment sourcing. Each aircraft in commercial service requires multiple avionics systems — including flight management computers, weather radar, traffic collision avoidance systems, communication radios, and navigation receivers — creating a high-value, recurring revenue stream for avionics manufacturers.

Regulatory mandates from EASA are a primary engine of commercial segment growth. The Single European Sky ATM Research (SESAR) initiative is progressively imposing new avionics capabilities on commercial operators, including advanced 4D trajectory management, data-link communications, and enhanced surveillance transponder performance. Compliance deadlines are non-negotiable for operators wishing to access EU airspace, translating directly into capital expenditure commitments for avionics upgrades.

Airbus, headquartered in Toulouse, France, plays an outsized role in shaping the commercial avionics demand curve. The Airbus A320neo family, A330neo, and A350 programs each incorporate sophisticated avionics suites sourced primarily from European suppliers, creating a virtuous procurement loop that benefits regional manufacturers. Honeywell International Inc has a significant presence in commercial avionics supply, providing cockpit systems and navigation solutions across multiple Airbus platform generations. Thales similarly holds substantial content on Airbus platforms, particularly in flight management and communication systems.

The commercial segment's share is not merely holding steady — it is growing in absolute terms as the new-build rate at Airbus accelerates. The manufacturer has publicly committed to ramping single-aisle production toward 75 aircraft per month by the mid-decade, each aircraft requiring a full avionics complement. This ramp translates into sustained forward order books for avionics suppliers, providing revenue visibility that extends well beyond the immediate forecast horizon.

Retrofit activity within the in-service commercial fleet constitutes an equally important revenue pillar. The average age of European commercial aircraft fleets makes many airframes candidates for avionics mid-life upgrades, particularly to satisfy connectivity mandates, cybersecurity hardening requirements, and fuel efficiency optimization through improved flight management algorithms. Cabin connectivity avionics, while distinct from flight-critical systems, are also generating incremental revenue as airlines compete on passenger experience metrics.

Key players dominating this segment include Thales, Honeywell International Inc, Safran, and RTX Corporation, each leveraging long-standing relationships with European OEMs and operators. The segment's growth is expected to consolidate around these incumbents due to the exceptionally high certification barriers that protect established avionics suppliers from new market entrants. The commercial aircraft segment's combination of regulatory pull, OEM demand, and retrofit volume secures its position as the uncontested leader within the broader European avionics landscape through 2033.